January 20, 2021

Dr Shane Oliver

Head of Investment Strategy and Economics and Chief Economist

(AMP Capital)

Whatever it is, the way you tell your story online can make all the difference.

Source: Bloomberg, FXStreet, AMP Capital

Investment markets and key developments over the past week

Global share markets were mostly down over the last week with US shares down 1.5% and European shares down 1.2% partly on profit taking after a run of strong gains along with concern about higher bond yields and soft economic data on the back of rising new coronavirus cases. Chinese shares also fell 0.7% for the week but Japanese shares rose 1.4%. Consistent with the soft US lead Australian shares fell 0.6% with gains in energy, financial and IT stocks being more than offset by falls in consumer staple, health and industrial shares. Bond yields were generally flat to down slightly but rose in Italy on new political turmoil there. Oil and iron ore prices rose slightly but gold and metal prices fell. The Australian dollar fell as the US dollar rose.

There was no let-up in the rising trend in new coronavirus cases globally over the last week, with the spread of the more contagious UK, South African and now Brazilian strains not helping. There may be some signs of a slowing in the US and Europe though, particularly in the UK, following the latest lockdowns but it’s too early to be sure. Even China has seen a pickup again leading to tighter restrictions/lockdowns in some areas, but the numbers are relatively low and no different to what it’s been seeing over the last six months in terms of occasional flare ups.

Whatever it is, the way you tell your story online can make all the difference.

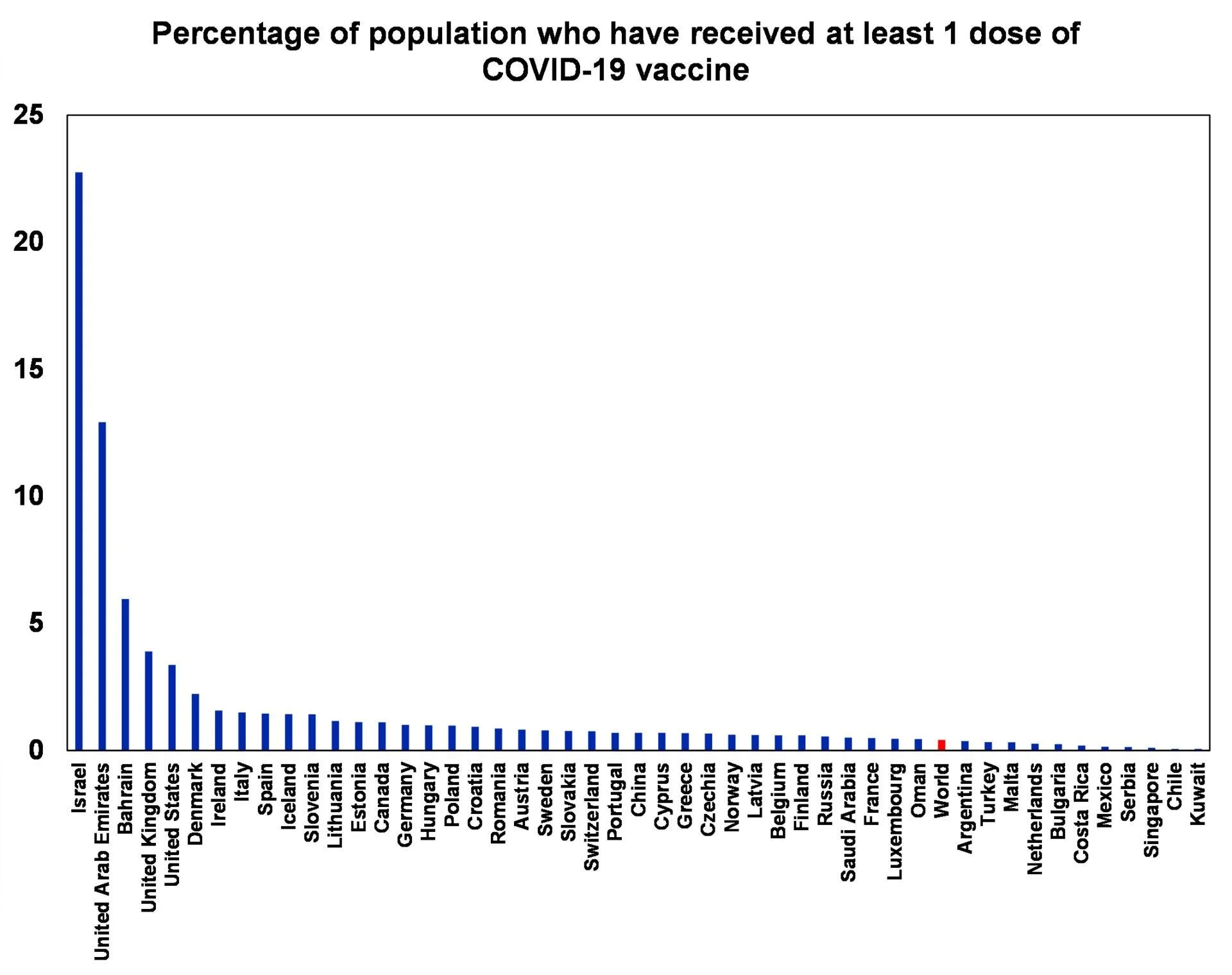

Source: ourworldindata.org, AMP Capital

Fortunately, vaccines are now starting to be rapidly deployed with Israel way out in front having vaccinated at least 20% of its population (which will provide a useful early guide as to the Pfizer vaccine’s real time effectiveness). There is also some evidence of a negative correlation between new hospitalisations and the percentage of the population having been vaccinated across US states. There is a long way to go though before the 70% or so level necessary for herd immunity will have been reached. In the US this is expected for around July/August. In Australia it will take longer as a smaller proportion of the population has been exposed to the virus, the start of the vaccine rollout is not till mid-February and there will be a greater reliance on the Astra-Zeneca vaccine which appears to be less effective on the basis of some tests.

Whatever it is, the way you tell your story online can make all the difference.

Source: ourworldindata.org, AMP Capital

In Australia, various coronavirus outbreaks appear to have been brought under control and despite concerns about the UK and South African variants escaping into the community the number of new local cases remains low. It remains too early to relax though given the ongoing return of international travellers and the greater risk of the more contagious versions escaping into the community via the traveller quarantine program.

Whatever it is, the way you tell your story online can make all the difference.

Source: covid19data.com.au, AMP Capital

So far the national economic impact of the tighter restrictions and brief mini lockdowns seen over the last month (including border closures) are likely to have been minor and not enough to derail the economic recovery (albeit its horrible for those businesses and workers that are directly affected). And if new cases remain low this will remain the case.

Consistent with this, while our weekly Economic Activity Tracker for Australia has fallen from its highs of late last year it has held up pretty well and remains relatively strong. By contrast our European Economic Activity Tracker remains very soft despite a bounce in the last week. And our US Tracker is continuing to trend down at a weak level and is pointing to a slowing in economic conditions since September.

Whatever it is, the way you tell your story online can make all the difference.

Source: AMP Capital

Political drama continuing in the US – but with little impact on investment markets providing the economic impact remains insignificant. The past week has seen the House impeach President Trump – making him the only president to be impeached twice – for inciting the Capitol riots that led to loss of life, with the vote including several Republicans and some abstentions. It now goes to the Senate but an outcome won’t occur until after Trump leaves office which is probably a good thing in terms of avoiding further inflaming tensions before Biden’s inauguration on Wednesday and in terms of helping to ensure perceptions of a fair trial. If convicted by the Senate, Trump would be prohibited from receiving benefits that normally go to former presidents and on a simple majority vote in the Senate could be prohibited from running again for office. Time will tell whether the necessary 67 senators will agree to convict him as this will require 17 Republican senators – although indications are that several are leaning in that direction. In the week ahead there are likely to be more protests with a high risk of violence, but provided this does not significantly impact economic activity and/or disrupt the political process then it’s unlikely to have much impact on investment markets. This was also the message from the Black Lives Matter protests in mid-year and past incidents such as the Oklahoma City bombing and the Atlanta Olympic Park bombing. While the drivers of extreme social divisions in the US – such as inequality – remain, the Democrats clean sweep of the Presidency, House and Senate along with Republicans now being weakened, point to a strong effort by the Biden Administration to deal with them over the next few years. Moderate Democrat senators will prevent a big left-ward lurch but significant extra fiscal stimulus with the initial tranche focussed on pandemic relief followed by more spending on infrastructure and dealing with climate change along with an expansion of Obamacare, a rise in the minimum wage and a small increase in the corporate tax rate (to 25%) and an increase in the top tax rate are likely. US shares will benefit from more stimulus, but the higher corporate tax rate will make non-US shares relatively more attractive.

In terms of the pandemic relief stimulus, President elect Biden’s announcement of a $1.9 trillion plan is more than expected but its passage through Congress is likely to see this cut back to around $1.2-1.5 trillion. Key elements include $1,400 stimulus cheques, state aid, an extension of unemployment insurance, small business and rental support and an increase in the minimum wage to $15/hr. Note that this is really just an ambit claim as it’s very hard to see all of this getting the support of 60 Senators and if the budget reconciliation process (which only requires a simple Senate majority but must be budget neutral over ten years) is used as is likely then moderate Democrat senators will likely scale it back to around $1.2-1.5 trillion. Another plan focused on infrastructure, climate and other longer-term goals will come later. Note that this is all gross spending. Tax hikes are to be expected – and probably necessary under the budget reconciliation process which will be required if Biden can’t get 60 senate votes, although moderate Democrats will limit them – which will reduce the ultimate size of the net stimulus, but for this year it’s still likely to be huge at around 10% of US GDP.

Taken together this will further boost US and hence global recovery which along with vaccines is likely to be stronger than generally expected, push share markets higher, favour non-US including Australian shares over US shares (as the US corporate tax rate goes up), push bond yields moderately higher, push the US$ down (and the A$ up) and favour cyclical value stocks over growth and defensive plays.

That said, share markets and other recovery plays like the Australian dollar and bond yields have run hard and fast since early November and remain vulnerable to a short term pull back. However, this should be viewed as just another correction before the rising trend resumes. The likelihood of 10% upside earnings surprise in the upcoming profit reporting seasons in the US and Australia should help limit any near-term share market correction.

Back to another round of political turmoil in Italy – but it doesn’t look likely to threaten the Euro beyond contributing to a possible short-term correction. Former PM Matteo Renzi’s Italy Alive party has withdrawn support for PM Giuseppe Conte’s coalition government. Italian bond yields backed up slightly in response and the Euro fell slightly. However, its unlikely to signal a return to Itexit (Italian exit of the Euro) worries seen a few years ago. First, revolving door Governments are the norm in Italy – Conte’s coalition at 16 months is actually older than the norm in Italy which has seen a new government every 15 months on average over the last 160 years. Second, the dispute is about government spending, power sharing and accessing the Eurozone’s emergency ESM fund and not about Euro membership. Conte may try to avoid a new election as centre right parties lead in the polls but even if one is called its unlikely to threaten the Euro as centre right parties are also pro Euro and EU fiscal stimulus has weakened populism. So, any blow out in Italy/German bond yield spreads and Euro weakness in response to related short-term uncertainty should ultimately prove to be a buying opportunity.

In Australia, there seems to be renewed concern about JobKeeper ending at the end of March. At this stage I don’t see it as being a major problem so long as the economy continues to recover. The number of jobs protected by JobKeeper has already collapsed from 3.6 million in September to 1.5 million in October because far less businesses met the criteria to continue receiving it. This is consistent with the unemployment rate having fallen further since September from 6.9% to 6.8%, in other words the 2.1 million reduction in jobs being supported by JobKeeper did not result in a rise in measured unemployment because the economy was recovering and businesses needed to keep the workers on. With Victoria reopening further since October the number of jobs needing protection is now likely to have fallen below 1 million and will likely have fallen further by March. This is also consistent with a collapse the number of workers working zero hours back to around pre-COVID levels. So, if the economy continues to recover by the time we get to April there may not be many still being protected by JobKeeper. There will still be some though, eg, in jobs dependent on international travel and foreign students but it’s likely to be far less than 100,000. The key to all of this is whether the economy continues to recover. So far it has recovered faster than expected despite the long Victorian lockdown and the latest coronavirus scare in the eastern states does not appear to have caused a major setback. If this remains the case, then the recovery is likely to continue and it will be appropriate to end JobKeeper as planned at the end of March. Alternatively, if a resurgence in coronavirus necessitating more severe lockdowns occurs threatening the recovery then I suspect that the Government will either extend JobKeeper (as it did beyond September) or announce a replacement. At this stage this appears unlikely though but there is no need for the Government to make a decision for another month or two.

Watching the brilliant Queen’s Gambit I was reminded what a classic Mason William’s 1968 instrumental Classical Gas is. One of the best versions is this one from Glen Campbell. Such a great guitarist, and he was even briefly one of The Beach Boys. Excellent as it was Classical Gas wasn’t the biggest instrumental hit of 1968 in the US with Paul Mauriat’s orchestral version of Love is Blue being number one for five weeks, which until 2017 was the only performance by a French artist to make it to number one in the US. Both are great head candy.

Major global economic events and implications

US economic data was soft on the back of rising new coronavirus cases and tightening restrictions. December industrial production rose solidly but retail sales fell again, small business optimism fell, manufacturing conditions in the New York region slowed in January, measures of consumer sentiment fell, job openings fell and there was a sharp rise in initial jobless claims. The Fed’s Beige Book of anecdotal evidence also noted a slowdown in economic activity in most districts. CPI inflation rose by more than expected driven by higher fuel and food prices, but underlying inflation remained weak as did underlying producer price inflation. Consistent with this, Fed officials, including Fed Chair Powell, pushed back against talk of an early tapering of bond buying in order to slow the rise in bond yields with Powell noting that “now is not the time to be talking exit” and “we are a long way from maximum employment”. Note though that March quarter GDP is likely to be boosted by the $900bn stimulus package now being dispersed which will particularly benefit households.

Eurozone industrial production rose more than expected in November and is almost back at pre-coronavirus levels, although lockdowns are likely to see it slow in December.

Japanese economic sentiment fell in December according to the Economy Watchers Index, likely in response to Japan’s third wave of coronavirus cases.

China’s trade data saw an acceleration in imports but slightly slower (but still strong) exports and some slowing in money supply and credit growth, albeit to still very high levels. Expect a further gradual slowing in credit growth as monetary policy normalises. Meanwhile headline CPI inflation rose back into positive territory and producer price deflation eased but core CPI inflation fell further to a weak 0.4%yoy.

Australian economic events and implications

Australian economic data was strong with a rise in the ABS’ measure of job vacancies for November to above their pre-COVID level consistent with an ongoing recovery in employment, housing finance surging to a new record high consistent with an ongoing recovery in house prices and retail sales confirmed at up 7% in November. Of course this is all before the latest COVID scare and resultant mini-lockdowns in late December/January but so far these don’t appear to have dramatically impacted economic activity based on our Economic Activity Tracker as consumer confidence has held up reasonably well and growth in credit and debit card transactions remains strong.

Whatever it is, the way you tell your story online can make all the difference.

Source: ABS, AMP Capital

Meanwhile, the Melbourne Institute’s Inflation Gauge rose solidly in December, but the trimmed mean remained weak at 0.1% month on month or 0.4% year on year pointing to ongoing weak underlying inflation pressures beyond rising prices for some things like petrol and insurance.

Whatever it is, the way you tell your story online can make all the difference.

Source: MI, AMP Capital

What to watch over the next week?

In the US, Joe Biden will be inaugurated as President on Wednesday which may see further violent protests from Trump supporters. On the data front expect gains in January home builder conditions (also Wednesday) and housing starts for December (Thursday) and the January composite business conditions PMI (Friday) will be a watched for any pull back from strong conditions in response to the surge in coronavirus cases and associated lockdowns.

US December quarter earnings reports will also start to flow. While consensus estimates are for a 9% year on year decline, strong business conditions readings point to a roughly flat outcome with early reporters already beating by around 10%.

The ECB on Thursday is expected to leave monetary policy very easy having extended its quantitative easing and cheap bank lending programs in December and January business conditions PMIs (Friday) are likely to remain soft given the ongoing increase in new coronavirus cases.

The Bank of Japan on Thursday is also expected to leave monetary policy very easy, Japanese CPI data for December (Friday) is expected to show continuing deflation and business conditions PMIs for January (also Friday) are expected to remain soft given the increase in new coronavirus cases.

Chinese GDP for the December quarter (Monday) is expected to show a continuing expansion with a 2.5% quarter on quarter gain resulting in four quarter ended GDP growth accelerating further to 6.2%yoy from 4.9%. For the whole of 2020 this will leave GDP up 2.1%. Economic activity data for December is expected to show continuing strength in industrial production at 6.9%yoy and a further acceleration in retail sales growth to 5.5%yoy and in investment growth

In Australia, expect a slight pullback in the Westpac/MI consumer confidence index for January (due Wednesday) from the 10 year high reached in December as a result of the renewed coronavirus scare over the last month, December jobs data (Thursday) to show a 25,000 gain with unemployment unchanged at 6.9%, the composite business conditions PMI for January (Friday) to fall back slightly but to a still strong 55 and flat December retail sales (also Friday) after the 7.1% gain seen in November and with coronavirus restrictions providing a bit of a dampener later in the month.

Outlook for investment markets

Shares are at risk of a short-term correction after having run up so hard recently and 2021 is likely to see a few rough patches along the way (much like we saw in 2010 after the recovery from the GFC). But looking through the inevitable short-term noise, the combination of improving global growth helped by more stimulus, vaccines and low interest rates augurs well for growth assets generally in 2021.

We are likely to see a continuing shift in performance away from investments that benefitted from the pandemic and lockdowns – like US shares, technology and health care stocks and bonds – to investments that will benefit from recovery – like resources, industrials, tourism stocks and financials.

Global shares are expected to return around 8% but expect a rotation away from growth heavy US shares to more cyclical markets in Europe, Japan and emerging countries.

Australian shares are also likely to be relative outperformers helped by better virus control, enabling a stronger recovery in the near term, stronger stimulus, sectors like resources, industrials and financials benefitting from the rebound in growth and as investors continue to drive a search for yield benefitting the share market as dividends are increased resulting in a 4.4% grossed up dividend yield. Expect the S&P/ASX 200 Index to end 2021 at a record-high of around 7200.

Ultra-low yields and a capital loss from a 0.5-0.75% or so rise in yields are likely to result in negative returns from bonds.

Unlisted commercial property and infrastructure are ultimately likely to benefit from a resumption of the search for yield but the hit to space demand and hence rents from the virus will continue to weigh on near term returns.

Australian home prices are likely to rise another 5% or so this year being boosted by record low mortgage rates, government home buyer incentives, income support measures and bank payment holidays but the stop to immigration and weak rental markets will likely weigh on inner city areas and units in Melbourne and Sydney. Outer suburbs, houses, smaller cities and regional areas will see relatively stronger gains in 2021.

Cash and bank deposits are likely to provide very poor returns, given the ultra-low cash rate of just 0.1%.

Although the A$ is vulnerable to bouts of uncertainty about coronavirus and China tensions and RBA bond buying will keep it lower than otherwise, a rising trend is still likely to around US$0.80 over the next 12 months helped by rising commodity prices and a cyclical decline in the US dollar.

Important notes

While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) (AMP Capital) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent of AMP Capital.