Dr Shane Oliver

Head of Investment Strategy and Economics and Chief Economist

(AMP Capital)

Investment markets and key developments over the past week

Share markets pushed higher again over the past week on the back of a declining number of new coronavirus cases in several countries raising the prospect of a relaxation in shutdowns, as policy stimulus measures continued to provide confidence that the economic downturn may be relatively short and as talk of a cut in global oil production boosted energy shares. US shares rose 12.1% for their best week since 1974, Eurozone shares gained 8.8%, Japanese shares rose 7.9% and Chinese shares rose 1.5%. While Australian banks were hit on talk of dividend suspensions, Australian shares rose 6.3% for the week helped by the strong global lead, with particularly solid gains in property and energy shares. From their lows around 23rd March, US shares are up 25% and have reversed nearly half of their plunge, global shares are up 22% and Australian shares are up 19%. Consistent with improved investor sentiment, bond yields rose as did copper and iron ore prices and the A$ rose above US$0.63 as the US$ fell. The oil price fell though on doubt as to whether oil production cuts would be enough to offset the slump in global oil demand.

The past week yet again saw a continuing rise in the number of coronavirus cases globally, a still rising death rate (it’s now 12.7% in Italy and 11.7% in the UK) and bleaker economic data. But there continues to be better news at the margin regarding the virus, notably in hot spots like Italy and even New York City, and in Australia.

While the total number of reported coronavirus cases is continuing to rise, the number of new cases may be levelling off (although it’s complicated by a big spike in French cases).

Source: Worldometer, Bloomberg, AMP Capital

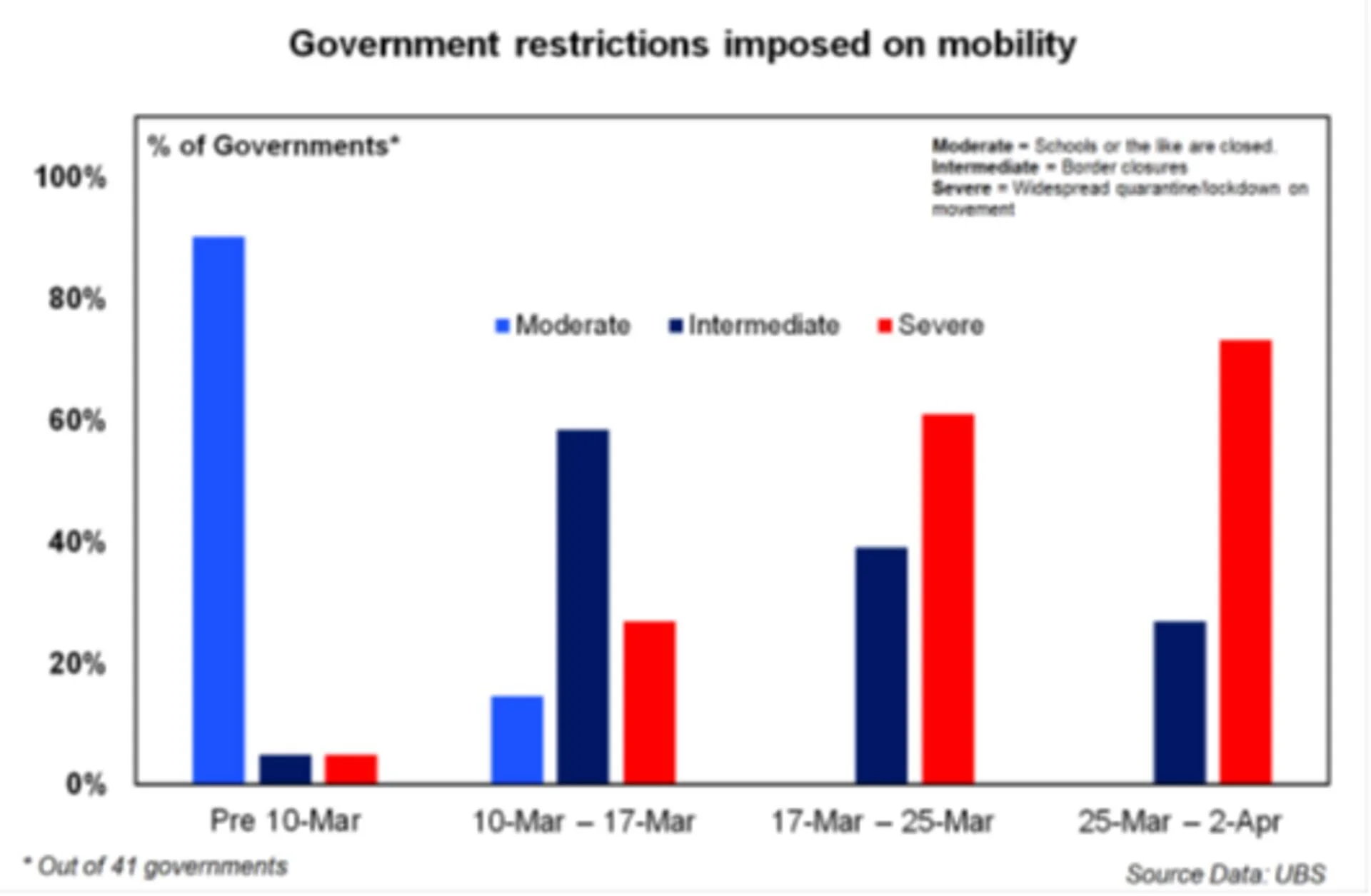

This may reflect increasing stringency in lockdowns globally. Nearly 80% of 41 major countries now have severe lockdowns in place, including Australia. While this means short term economic pain, it also means a greater chance of controlling the virus earlier.

Source: UBS, AMP Capital

There is increasing evidence that this is working in Europe. While France still looks problematic, a downtrend in new cases is evident in Italy, Spain, Germany, the Netherlands, Austria and Switzerland.

Source: Worldometer, Bloomberg, AMP Capital

While the US is still seeing a rising trend, the number of new cases in New York has slowed.

Australia is now clearly seeing a downtrend in new cases in response to social distancing policies. In fact, this appears to be occurring faster than the Government had assumed. As a former journalist friend observed, “maybe Australia slipped on a banana peel just as the bullet was about to hit.” Or it’s down to less congested living and warmer weather. Then again, that’s probably too cynical given the lockdown that has been put in place and enforced.

Source: Worldometer, AMP Capital

This has seen Australia’s total number of cases per million people remain low and is not dissimilar to Asian countries that have been relatively successful in stabilising the number of cases.

Source: Worldometer, AMP Capital

Out of interest, a ranking of how well countries have grappled with coronavirus based on the percentage of cases that have recovered, total cases relative to the outbreak’s duration, active cases per capita and tests per capita ranks Australia at number 3, behind only China and South Korea out of 30 countries. Italy is ranked 22nd, the US is ranked 23rd and the UK is ranked very poorly at 27th.

With parts of Europe and Australia now following a similar pattern with new cases to that experienced by China (that saw a peak in new cases around 11 to 21 days after its lockdown), it’s possible that like China they will be able to start relaxing the lockdown in a month or so. Of course, in the absence of a vaccine a full relaxation would be unwise, given the risk of a second wave of infections (like in 1918 with Spanish Flu), but providing international travel remains banned (removing the threat of imported cases) and any low level community transmission cases are rigorously quarantined and contacts traced, then some relaxation will be likely. Of course, we have to keep the number of cases going down. If this is the case, then economic activity should bottom this quarter, allowing the start of a gradual recovery through the second half. Fingers crossed! Mass testing of the population that shows a high level of antibodies to COVID-19 and hence significant “herd immunity” may permit a faster and more confident relaxation, but such testing is still a way off.

Meanwhile, policy support continued to ramp up over the last week and this is continuing to help tip the risks away from coronavirus shutdowns causing a long and extended recession/depression.

US political leaders are now working on another stimulus package to be at least US$1 trillion (4.5% of GDP).

The US Federal Reserve (Fed) massively ramped up its coronavirus-related lending programs to $2.3 trillion, leveraging $454 billion in US Treasury risk capital that was allocated from the recently-passed Federal stimulus program. This includes lending to small and medium enterprises and to state and local governments, as well as the purchase of investment grade and some high-yield bonds (where an investment grade credit rating was lost due to the crisis), collateralised loan obligations and commercial mortgage-backed securities. Fed Chair Powell indicated the central bank will act “forcefully, proactively and aggressively until we are confident we are solidly on the road to recovery”. He also noted other tools may also be considered.

Japan announced a new US$1 trillion stimulus package that contains roughly 3.5% of GDP in spending (as opposed to loans).

European Union (EU) finance ministers finally agreed to a €540 billion support package designed particularly to help countries with weaker fiscal positions. Relying mainly on the European Stability Mechanism and the European Investment Bank, it’s not quite as strong as might have been hoped for and there are still no common bonds. This will leave the European Central Bank (ECB) continuing to play an outsized role. But it’s still a big move in the right direction.

The ECB announced that it will reduce its credit standards for lending through the crisis. This will further encourage access to its cheap bank funding program and make it easier for countries like Greece.

The UK looks to have crossed a line into actual helicopter money with the Bank of England providing “temporary and short term” financing for the Government. Maybe its temporary and just to smooth out financing for the UK’s virus programs but still!

“Whatever it takes” to limit the impact on the economy and ensure a decent recovery remains the mantra of global policy makers (albeit the EU remains a bit of a laggard). If actual and currently proposed spending and tax break measures are allowed for, global policy stimulus is now running over 4% of global GDP, far greater than seen in the GFC. Note that this does not include government lending or loan guarantees, which may turn out to be “spending”.

Source: IMF, AMP Capital

It’s still too early to say that shares have bottomed as there is still a lot of bad news to come. But increasing policy support, against the backdrop of increasingly positive signs that suppression is working and it may be possible to relax lockdowns in the next month or so, are positive signs that we have seen the low – or have come close to the low.

I haven’t had a song in here for a while now. What the world needs now is love is one of my favourites. At times like these its particularly relevant.

Major global economic events and implications

In the US, data for small business confidence, consumer confidence and mortgage applications for new home purchases all fell sharply, reflecting the impact of coronavirus shutdowns. Jobless claims surged another 6.6 million, bringing the total rise over the last 3 weeks to around 17 million, but note that if March is any guide more than 80% of these are on temporary layoffs. Meanwhile, March CPI inflation fell more than expected. The minutes from the Fed’s two March meetings added little that was new, but confirm that the Fed sees the virus shock as reducing inflation. On the political front, it was no surprise to see Bernie Sanders drop out of the Democratic Party’s presidential nomination race, leaving a clear run for the more business-friendly Joe Biden.

Japanese consumer confidence and the Economy Watcher’s household and business conditions indicators fell sharply in March.

Chinese CPI inflation fell to 4.3% year-on-year in March, with slower food prices. Core inflation was just 1.2% year-on-year and producer prices fell 1.5% year-on-year. The coronavirus crisis is more deflationary than inflationary. Meanwhile, money supply and credit growth accelerated much more than expected in March, likely reflecting policy easing.

Australian economic events and implications

Australian data releases are now increasingly starting to show the impact of the coronavirus shutdown. Housing finance commitments for February fell for the first time since May last year. The February trade surplus narrowed as a 15% slump in tourism (as Chinese tourists were banned) drove a slump in exports, which was partly offset by a slump in imports. An ABS survey reported 66% of businesses seeing reduced turnover thanks to the shutdowns (up from 49% the week before) and ANZ job ads plunged 10% in March as the labour market starts to weaken. Unfortunately, none of this is really surprising and there is worse to come. For those worried about inflation, the Melbourne Institute’s Inflation Gauge for March remained soft at 1.5%, with underlying inflation actually falling to 1.2% (higher prices for toilet paper perhaps but not much else!).

As widely expected, the Reserve Bank of Australia (RBA) made no further changes to monetary policy at its regular board meeting and just reaffirmed the emergency measures it made three weeks ago. It did note though that financial markets appear to be working better than three weeks ago and, if conditions continue to improve, its bond buying and open market operations may be smaller going forward. This should be seen as a sign of success though, rather than reflecting reduced RBA support for markets, and is similar to what the Fed has been doing. More RBA action may still be needed though.

In its latest Financial Stability Review, the RBA signalled a reasonable degree of confidence in the Australian financial system’s ability to withstand the coronavirus crisis, noting that it’s in a strong starting position with high capital levels and improved bank liquidity. While it noted the “longstanding risks” around high household debt levels and elevated home prices, it sees significant financial buffers for some households, repayment holidays and the wage subsidy as helping limit arrears. It also noted that Australian businesses mostly have low gearing levels.

The cut by S&P to Australia’s AAA sovereign credit rating outlook to negative on the back of the Government’s fiscal stimulus is unlikely to have much impact on Australian borrowing costs. Historically, bond yields have gone the opposite direction to implied moves from a rating change about half the time. I would rather the Government risk a rating downgrade than a prolonged depression/recession any day! Ratings are really a relative game and Australia’s public debt-to-GDP ratio will remain well below that of other major countries who are also undertaking fiscal stimulus.

What to watch over the next week?

The number of new COVID-19 cases, lockdowns and their economic impact and the global policy response to deal with it will likely remain the focus. Key metrics to watch for remains a continuing downtrend in new cases in Italy and a peak, hopefully soon, in the number of new cases the US. Economic releases will show the increasing impact of coronavirus shutdowns.

In the US, expect to see sharp falls in March data for retail sales, industrial production and home builder conditions (Wednesday) and similarly sharp falls in March housing starts and permits and another big rise in jobless claims (Thursday). The New York and Philadelphia regional manufacturing conditions surveys for April are also likely to be very weak. The flow of March quarter earnings reports will ramp up and are likely to show a sharp fall as shutdowns impact with negative/uncertain outlook comments.

In China, March quarter GDP (Friday) is expected to show a fall of 10% quarter-on-quarter or -6% year-on-year, reflecting the shutdown seen through late January and February. Meanwhile, expect to see an improvement in momentum in activity data for March as the shutdown eased, allowing a gradual recovery with industrial production down 6.4% year-on-year but up from a fall of 13.5% year-on-year over January and February, retail sales down 6.5% year-on-year but up from -20.5% and investment down 14.5% but up from -24.5%. Trade data (Tuesday) is likely to show continuing weakness in exports and imports. Credit data is also due for release.

In Australia, expect to see a sharp fall in the NAB survey measures of business conditions and confidence (Tuesday) and the Westpac/MI survey measure of consumer confidence (Wednesday). Jobs data for March (Thursday) is expected to show a 50,000 loss in employment and a rise in unemployment to 5.5%.

Outlook for investment markets

Shares have had a great rally from the lows in March but it’s still too early to say we have seen the bottom, given the uncertainty around the coronavirus both in terms of the outbreak’s duration and its economic impact. But on a 12-month horizon, shares are expected to see good total returns, helped by an eventual pick-up in economic activity and massive policy stimulus.

Low starting point yields are likely to result in low returns from bonds once the dust settles from coronavirus.

Unlisted commercial property and infrastructure are ultimately likely to continue benefitting from the search for yield, but the hit to economic activity from the virus will weigh heavily on near-term returns.

The Australian housing market is now weakening rapidly in response to coronavirus. Social distancing will drive a collapse in sales volumes, while a sharp rise in unemployment, a stop to immigration through the shutdown and rent holidays pose a major threat to property prices. Prices are expected to fall between 5% to 20%, but government support measures – including wage subsidies along with bank mortgage payment deferrals – coupled with a plunge in listings will help limit falls at least for the next six months.

Cash & bank deposits are likely to provide very poor returns, given the ultra-low cash rate of just 0.25%.

The hit to global growth from COVID-19 and its flow on to reduced demand for Australian exports and lower commodity prices still risks pushing the A$ lower in the short term, possibly to a re-test of its low three weeks ago of US$0.55. But expect a strong rebound once the threat from coronavirus recedes.