Shane Oliver, Head of Investment Strategy and Chief Economist

The attached note looks at the ongoing threat posed by coronavirus to global growth and investment markets. The key points are as follows:

The rout in financial markets has continued, on the back of coronavirus, made worse by a flow on to oil markets.

The risk of a deeper hit to economic activity has risen. Key things to watch are the daily number of new cases, measures of economic stress and policy stimulus.

Key things for investors to bear in mind remain that: share market falls are normal; selling shares after a fall locks in a loss; share pullbacks provide opportunities; and to avoid getting thrown off a long-term strategy it's best to turn down the noise during times like this.

Introduction

Coronavirus continues to rattle investment markets as the number of new cases outside China continues to rise posing increasing uncertainty over the impact on economic activity. And its impact has intensified following the collapse of OPEC discipline causing a further plunge in oil prices raising concerns about debt servicing for oil producers. From their highs global shares and Australian shares have had a fall of around 20%.

Source: PRC National Health Commission, Bloomberg, AMP Capital

Given the extreme uncertainty this note looks at various scenarios in relation to global and Australian economic growth and what signposts to look at in relation to how it may unfold.

Much ado about nothing or a major global catastrophe

It seems there are two extreme views on coronavirus. Some see it as just a bad flu and can’t see what the fuss is all about. Others think that it will trigger a major humanitarian and economic catastrophe killing millions and triggering a major global recession as excessive leverage is finally exposed. The optimist in me wants to lean to the former:

So far over 114,000 people are reported to have contracted the virus of which nearly 4000 have died. Of course, this number is still growing but in China where the number of new cases has collapsed (see the first chart) the number is 80,754 cases and 3136 deaths. In the 2017-18 US flu season alone 44.8m Americans got sick and 61,099 died.

The actual death rate from Covid-19 may be 1% or lower, rather than the currently reported rate of 3.5% because many of those who get the virus don’t get sick enough to seek medical help and so won’t be included in the case count. The Diamond Princess episode may provide a rough guide – all 3711 passengers and crew have been tested with 705 contracting the virus of which seven have died and most of those are believed to have been over 70. This would suggest a death rate of around 1% which is only just above that for regular flu for those over 65.

It appears to be less contagious than regular flu.

China’s experience shows it can be contained. Maybe this is due to extreme containment measures in Hubei that are not possible in other countries. But the case count in the rest of China has also been contained with less extreme measures and Singapore and Hong Kong have had some success in slowing new cases without extreme quarantining.

Source: PRC National Health Commission, Bloomberg, AMP Capital

Given the extreme uncertainty this note looks at various scenarios in relation to global and Australian economic growth and what signposts to look at in relation to how it may unfold.

Much ado about nothing or a major global catastrophe

It seems there are two extreme views on coronavirus. Some see it as just a bad flu and can’t see what the fuss is all about. Others think that it will trigger a major humanitarian and economic catastrophe killing millions and triggering a major global recession as excessive leverage is finally exposed. The optimist in me wants to lean to the former:

So far over 114,000 people are reported to have contracted the virus of which nearly 4000 have died. Of course, this number is still growing but in China where the number of new cases has collapsed (see the first chart) the number is 80,754 cases and 3136 deaths. In the 2017-18 US flu season alone 44.8m Americans got sick and 61,099 died.

The actual death rate from Covid-19 may be 1% or lower, rather than the currently reported rate of 3.5% because many of those who get the virus don’t get sick enough to seek medical help and so won’t be included in the case count. The Diamond Princess episode may provide a rough guide – all 3711 passengers and crew have been tested with 705 contracting the virus of which seven have died and most of those are believed to have been over 70. This would suggest a death rate of around 1% which is only just above that for regular flu for those over 65.

It appears to be less contagious than regular flu.

China’s experience shows it can be contained. Maybe this is due to extreme containment measures in Hubei that are not possible in other countries. But the case count in the rest of China has also been contained with less extreme measures and Singapore and Hong Kong have had some success in slowing new cases without extreme quarantining.

Source: PRC National Health Commission, Bloomberg, AMP Capital

Alternatively, at some point authorities outside China may just conclude that containment is impossible and, as the death rate is not apocalyptic, shift from containment to just treating those who get very sick. This could enable life to return to normal, albeit with a change in behaviour – less handshaking, frequent handwashing and wearing a mask.

But I also must concede I just don’t know. There is much that is unknown about the virus itself and how long it will continue to spread. And even if there is a switch to just treating the very sick it’s unclear there will be enough hospital beds. And there is also the human or behavioural overlay which is intensifying the economic impact. Just look at the toilet paper frenzy to see that this can have a real economic effect even before the virus has really taken hold in Australia. While there may be a boom in demand for hand sanitisers, toilet paper and long-life food, this will be a temporary boost as the spread of the virus globally and the disruption that containment measures are causing is continuing to increase the risk of a longer and deeper hit to economic activity. And there is a risk of secondary effects as the short-term disruption risks leading to business failures and households defaulting on their debts if they can’t keep up their payments and so causing a deeper impact on economic activity. The secondary effects of the coronavirus outbreak and its flow on is highlighted by the 45% collapse in oil prices since mid-January. Ultimately lower petrol prices will be a good thing as this will boost consumer spending when the virus goes away but for now all the focus is on the downside of lower oil prices – debt problems and less business investment by producers.

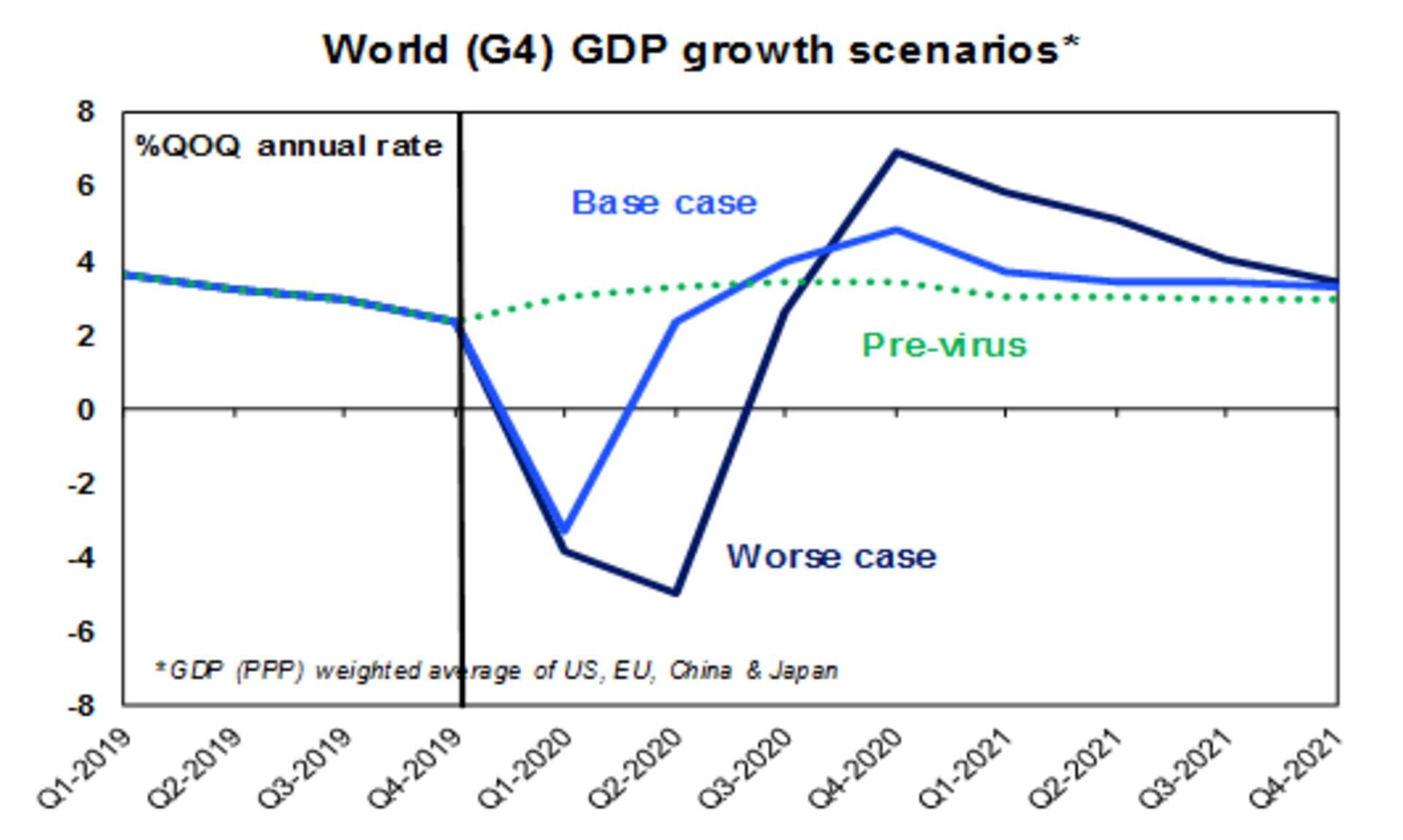

Base case versus global recession and beyond

Given all these uncertainties it’s still too early to say that shares, commodity prices and bond yields have bottomed. The following charts present three scenarios for the global economy:

How we saw global growth panning out prior to the virus. Basically, we were expecting a mild pick-up in growth.

A sharp downturn centred around the March quarter as the Chinese economy contracts sharply but rebounds in the June quarter offsetting recessions in developed countries including in the US. This is our base case.

A worse case downturn that sees global growth contract in the March quarter (led by a sharp contraction in China) and the June quarter as (as developed countries get badly hit) resulting in a global recession to be then followed by a rebound as life returns to normal led by China.

Note: the scenarios show quarterly annualised growth. The key is to focus on the pattern of growth rather than the precise level.

Source: Bloomberg, AMP Capital

The next chart shows three scenarios for Australian growth:

How we saw global growth panning out prior to the virus.

Mild downturns in the March and June quarters driven initially by the lockdown in the China and then the coronavirus flow on to the rest of the world and Australia, followed by a second-half rebound. This is our base case.

A worse case downturn that sees deeper downturns in the March and June quarters then followed by a rebound as life returns to normal.

Source: Bloomberg, AMP Capital

Last week we moved to forecasting a recession for the Australian economy in our weekly report. We were already expecting a negative March quarter on the back of the bushfires and the hit to tourism, education exports and commodity exports from the slump in China. But the spread of coronavirus globally and in Australia has made it likely that we will also see a contraction in the June quarter too. As with the global outlook this should really be “a disruption” that will pass once the virus runs its course – hopefully at least as the Northern Hemisphere heads toward summer. The worse case scenarios would likely see a deeper decline in shares and bond yields.

What to watch?

Shares will bottom when there is confidence that the worst is over in terms of the economic impact from the virus and its largely factored in. So, the debate is largely now about how big the hit to growth will be and this relates to how long the virus will weigh on global growth and any secondary effects it may cause. In this regard the key things to watch are as follows:

A peak in the number of new cases – as per the first chart.

News of successful vaccines or anti-virals.

Whether governments switch from containment.

Timely economic indicators, eg, jobless claims and weekly consumer confidence data in the US and Australia.

Measures of corporate stress, eg, spreads between corporate bond yields and government bond yields.

Measures of household stress, eg, unemployment and non-performing loans.

Measures of market stress, eg, bank funding costs as measured by the gap between 3-month rates and central bank rates. These have risen but are well below GFC levels.

Source: Bloomberg, AMP Capital

The monetary and fiscal policy response – this will be critical in terms of minimising the impact on vulnerable businesses and households from the coronavirus disruption, ensuring financial markets remain liquid and driving a quick recovery once the threat from the virus is over. So far so good with policy makers moving in the right direction (rapidly so in Australia it seems) – but there is a fair way to go.

What does it all mean for investors?

The rapidity of the fall in share market has been scary. In our view the key things for investors to bear in mind are as follows:

periodic sharp falls in share markets are healthy and normal. With the long-term trend ultimately remaining up & providing higher returns than other more stable assets.

selling shares or switching to a more conservative investment strategy after a major fall just locks in a loss.

when shares fall, they are cheaper and offer higher long-term return prospects. So, the key is to look for opportunities the pullback provides. It’s impossible to time the bottom but one way to do it is to average in over time.

while shares have fallen, dividends from the market haven’t. Companies like to smooth their dividends over time – they never go up as much as earnings in the good times and so rarely fall as much in the bad times.

shares and other related assets bottom at the point of maximum bearishness, ie, just when you feel most negative towards them.

the best way to stick to an appropriate long-term investment strategy, let alone see the opportunities that are thrown up in rough times, is to turn down the noise.

Important notes

While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) (AMP Capital) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent of AMP Capital.