Investment markets & key developments

It was another volatile weak in share markets with worries that rate hikes, cost pressures and Chinese supply disruptions would hit profits after downgrades from some US retailers and tech stocks. For the week, this saw US shares fall 3.1% (which is their seventh weekly fall in a row) and Eurozone shares lose 0.7%, but Japanese shares rose 1.2%, Chinese shares rose 2.2% and Australian shares gained 1.0%, helped by monetary easing in China. In Australia, gains in IT, utility and material shares more than offset falls in consumer and energy shares. Bond yields fell in the US and Australia, but rose in Europe. Oil, metal and iron ore prices rose, as did the $A as the $US pulled back a bit.

From their bull market highs US shares are down 19%, led by the Nasdaq, which is down 29%, Eurozone shares are down 16%, Japanese shares are down 13%, global shares are down 16% & Australian shares are down 6%. Australian shares remain a relative outperformer thanks to their commodity exposure, despite the plunge in Chinese growth and their low exposure to tech stocks.

The inflation and rate hike drumbeat continued to reverberate over the last week, with more concern about a flow on to growth and profits:

US Federal Reserve (Fed) Chair Powell indicated that the Fed needs “clear and convincing” evidence that inflation is falling, 0.5% rate hikes remain on the table and there “could be some pain” in getting inflation down. At least the market has not further ratcheted up Fed rate hike expectations.

• Profit warnings from some US retailers and tech stocks as a result of cost increases and supply disruptions from China added to nervousness about the profit outlook.

• This was not helped by weak Chinese economic data for April, although it was partly offset by more policy easing.

• UK and Canadian inflation rose again in April to 9%yoy and 6.8%yoy respectively, leaving their central banks on track for more rate hikes.

• The minutes from the Reserve Banks of Australia’s (RBA) last meeting and strong jobs data left little doubt that the RBA will hike rates again in June. The RBA will be data dependent in determining when and by how far it will raise rates, but the clear message from the minutes are that it’s concerned about a rise in inflation expectations, it seriously considered a 0.4% hike this month and that more rate hikes are on the way. While March quarter wages growth was on the soft side, it was in line with RBA expectations and the tight labour market – with unemployment now at 3.85%, which is its lowest since 1974 – along with numerous business surveys and the RBA’s own business liaison, point to an acceleration in wages growth ahead. As a result, and given RBA concerns that inflation psychology might rise, it is likely to step up the pace of tightening in June in order to get on top of inflation. We expect a 0.4% hike, taking the cash rate to 0.75%. By year end, we continue to see the cash rate rising to between 1.5% and 2%. Having the unemployment at a 48-year low is great news, but it’s also a little ominous given the stagflation that followed when unemployment was last below 4% back in 1974. The key lesson from the 1970s is that the RBA needs to act quickly to make sure inflation expectations do not rise significantly, because if they do, it will be much harder to get inflation back down. So expect it to continue with rate hikes until it gets clear evidence that inflation will slow. Signs of an acceleration in the decline in home prices in Sydney and Melbourne will help in this regard, as falling home prices impact consumer demand and hence inflation via negative wealth effects, but there is a way to go yet.

Investment markets & key developments

It was another volatile weak in share markets with worries that rate hikes, cost pressures and Chinese supply disruptions would hit profits after downgrades from some US retailers and tech stocks. For the week, this saw US shares fall 3.1% (which is their seventh weekly fall in a row) and Eurozone shares lose 0.7%, but Japanese shares rose 1.2%, Chinese shares rose 2.2% and Australian shares gained 1.0%, helped by monetary easing in China. In Australia, gains in IT, utility and material shares more than offset falls in consumer and energy shares. Bond yields fell in the US and Australia, but rose in Europe. Oil, metal and iron ore prices rose, as did the $A as the $US pulled back a bit.

From their bull market highs US shares are down 19%, led by the Nasdaq, which is down 29%, Eurozone shares are down 16%, Japanese shares are down 13%, global shares are down 16% & Australian shares are down 6%. Australian shares remain a relative outperformer thanks to their commodity exposure, despite the plunge in Chinese growth and their low exposure to tech stocks.

The inflation and rate hike drumbeat continued to reverberate over the last week, with more concern about a flow on to growth and profits:

US Federal Reserve (Fed) Chair Powell indicated that the Fed needs “clear and convincing” evidence that inflation is falling, 0.5% rate hikes remain on the table and there “could be some pain” in getting inflation down. At least the market has not further ratcheted up Fed rate hike expectations.

Profit warnings from some US retailers and tech stocks as a result of cost increases and supply disruptions from China added to nervousness about the profit outlook.

This was not helped by weak Chinese economic data for April, although it was partly offset by more policy easing.

UK and Canadian inflation rose again in April to 9%yoy and 6.8%yoy respectively, leaving their central banks on track for more rate hikes.

The minutes from the Reserve Banks of Australia’s (RBA) last meeting and strong jobs data left little doubt that the RBA will hike rates again in June. The RBA will be data dependent in determining when and by how far it will raise rates, but the clear message from the minutes are that it’s concerned about a rise in inflation expectations, it seriously considered a 0.4% hike this month and that more rate hikes are on the way. While March quarter wages growth was on the soft side, it was in line with RBA expectations and the tight labour market – with unemployment now at 3.85%, which is its lowest since 1974 – along with numerous business surveys and the RBA’s own business liaison, point to an acceleration in wages growth ahead. As a result, and given RBA concerns that inflation psychology might rise, it is likely to step up the pace of tightening in June in order to get on top of inflation. We expect a 0.4% hike, taking the cash rate to 0.75%. By year end, we continue to see the cash rate rising to between 1.5% and 2%. Having the unemployment at a 48-year low is great news, but it’s also a little ominous given the stagflation that followed when unemployment was last below 4% back in 1974. The key lesson from the 1970s is that the RBA needs to act quickly to make sure inflation expectations do not rise significantly, because if they do, it will be much harder to get inflation back down. So expect it to continue with rate hikes until it gets clear evidence that inflation will slow. Signs of an acceleration in the decline in home prices in Sydney and Melbourne will help in this regard, as falling home prices impact consumer demand and hence inflation via negative wealth effects, but there is a way to go yet.

The last observation is for May month to date. Source: CoreLogic, AMP

The risks around inflation, monetary tightening, the war in Ukraine and Chinese growth remain high and still point to a further escalation in recession fears, and hence more downside in share markets before they bottom. We are also yet to see the extremes in investor sentiment as measured by the VIX index and Put/Call ratios normally seen at major market bottoms. Fortunately, our Pipeline Inflation Indicator continues to point to a peaking in inflation, which should take pressure of central banks later this year, or early next, in time to avoid recession. This in turn should enable share markets to be up on a 12-month view. The near-term risks remain high though.

The Inflation Pipeline Indicator is based on commodity prices, shipping rates and PMI price components. Source: Macrobond, AMP

Australian petrol prices back to March highs – So much for the fuel excise cut! While global oil prices are up again and the $A is down, this is not enough to explain the surge in petrol prices. See the next chart. Rather a rise in global refined petrol costs appears to be the main driver on the back of low stockpiles in the US ahead of the summer driving season. Even then petrol prices look to have overshot, particularly once allowance is made for 24 cents a litre fuel tax cut. It also highlights how the fuel tax cut can easily be overwhelmed by swings in the oil and petrol market. Now we have little to show for it, the ATO has lost the revenue it would have raised and it’s going to be really hard to raise it in September.

Source: Bloomberg, AMP

Australia has a new Government. While the count continues, the ALP looks set to form Government either in its in own right or as a minority government. Unlike in 2019, apart from climate change policies the economic policy platform of Labor is not dramatically different from that of the Coalition. Labor policies, including more spending on childcare and aged care, offset by various savings, imply slightly more net spending and slightly bigger deficits (of around $1.85bn or 0.1% of GDP a year), but there is not a lot in it and spending has already blown out under the Coalition. Labor’s “Help to Buy” scheme for new home buyers will, like all demand side housing schemes, simply add to upwards pressure on home prices, but with only 10,000 places a year the impact is likely to be marginal and it won’t head of a slump in property prices over the next year in response to rising interest rates. Labor policies don’t point to a real fix to housing affordability, although its promises for 30,000 social homes and a National Housing Supply Council may help a bit. A major concern is that Labor, the minorities and independents are not prepared for significant budget repair and the sort of economic reform agenda that will likely be necessary if inflation and interest rates remain higher for longer. But then again, neither was the Coalition. Governing in a world of higher inflation and interest rates will be the main challenge for the new Government.

Labor’s macro policies not being significantly different from the Coalition’s and the fact that polls have been pointing to a Labor victory, such that it’s not a surprise, suggest that the market reaction to the change of Government will be minor. The main risk for markets will come if Labor has to rely on the Greens to form Government and they push Labor down a far less business-friendly path than its election platform suggests, such as implementation of the Greens’ proposed super profits tax on business. However, there will now be plenty of “teal” independents in Parliament whose policies on climate, integrity and health align more closely with Labor and for whom Labor should be able to gain support from. This could result in a bit of uncertainty for the share market and the $A until its resolved. After the 2010 election in which neither of the major parties secured a majority, it took 17 days for the Gillard minority Government to be formed, with shares initially falling 2.5% over the first three trading days but rising 3.3% through the negotiation period as a whole.

A vote for the sensible centre. While there will no doubt be lots of political analysis about what the election result means in the weeks ahead, it seems that it represented a rejection of more right wing/conservative views on climate, women, health and integrity in support for what one of the new “teal” independent House of Reps members refers to as the “sensible centre”. Just as the 2019 election result represented a rejection of more left wing tax and spend policies in favour of the “sensible centre”. In this sense it may be seen as a good thing for centrist sensible policy making in Australia.

I just came across local band Lime Cordial in an endorsement for a local candidate in the Federal election, so checked them out. And they are kinda very cool. Here they are with No Plans To Make Plans, Facts of Life and Inappropriate Behaviour. I miss drive-ins! If you haven’t already – do yourself a favour and check them out.

Coronavirus update

New global COVID cases rose slightly over the last week, with increases in Asia and the US. New Omicron sub-variants warn of a further increase. However, while they are more transmissible, they do not appear more harmful, with vaccines still provide protection against serious illness.

Source: ourworldindata.org, AMP

This is consistent with South Africa’s experience with the new variants where hospitalisation and death rates have remained subdued compared to the pre-Omicron experience. New cases in South Africa may also be starting to slow.

Source: ourworldindata.org, AMP

China has seen a big slowing in new covid cases, which may allow for some easing in lockdowns. However, China may face a rough ride if it sticks to its zero Covid policy as Omicron is far harder to suppress than the original Covid virus.

Source: ourworldindata.org, AMP

The recent rise in new cases in Australia has rolled over again in the last few days. Hospitalisation and death rates are likely to remain low compared to pre-Omicron waves, helped by high rates of vaccination protecting against serious illness and the subvariants remaining mild.

Source: ourworldindata.org, AMP

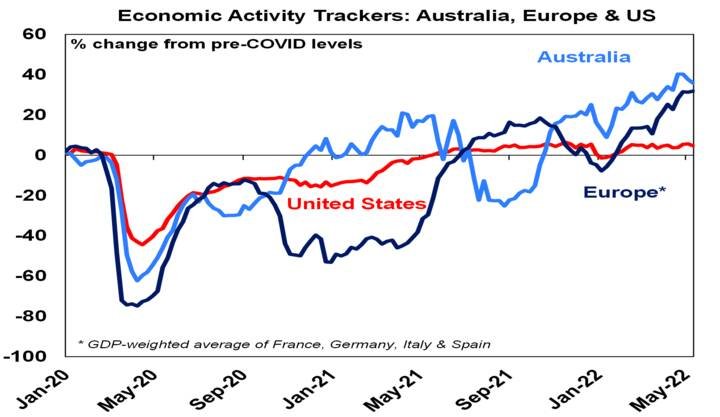

Economic activity trackers

Our Australian Economic Activity Tracker fell again over the last week but remains strong. Our European Tracker was little changed but the US fell a bit. Given the rising risk of recession our Economic Activity Trackers are worth watching as they are based on weekly data and so should give timely signals regarding the risk of recession.

Based on weekly data for eg job ads, restaurant bookings, confidence, mobility, credit & debit card transactions, retail foot traffic, hotel bookings. Source: AMP

Major global economic events and implications

US economic data was mixed over the past week. Retail sales and industrial production were strong in April but home builder conditions, home sales, housing starts and permits to build new homes fell, indicating that higher mortgage rates are starting to impact. Manufacturing conditions indexes in the New York and Philadelphia regions were also weak (although confusingly the details in the Philadelphia survey were actually strong, with shipments and new orders up), but at least delivery times improved and price indicators slowed a bit. Initial jobless claims also rose further, suggesting a cooling jobs market (which would be welcomed by the Fed) but continuing claims are still falling, suggesting workers are still having no trouble finding jobs.

95% of US S&P500 companies have now reported March quarter earnings, with 76% beating expectations, which is in line with the norm. However, consensus earnings expectations for the quarter have now moved up to 11.8%yoy from 4.3% at the start of the reporting season. Energy, materials and industrials are seeing the strongest earnings growth. Earnings growth in Europe & Asia has been stronger though, averaging 14.8%yoy. Profit downgrades from some retailers (Walmart and Target) warn of rising cost and margin pressures though.

Japanese March quarter GDP contracted by 0.2% as COVID restrictions impacted, but the decline was less than expected as consumer spending held up better than feared and GDP should bounce back this quarter. Core CPI inflation rose, but to a still low 0.8%yoy in April, as cuts to mobile phone rates a year ago dropped out of the annual inflation calculation. But producer price inflation surged to 10%yoy for the first time in 40 years, suggesting that Japanese CPI inflation could also rise more significantly in the months ahead after decades bouncing around zero, helped by a fall in the Yen and surge in global inflationary pressures. Which could point to a possible Bank of Japan (BoJ) tightening next year.

Chinese economic activity data was hit hard in April by COVID related lockdowns. Industrial production and retail sales fell, unemployment rose and home prices fell. Reflecting the downturn, mortgage rates were cut for first home buyers, the People’s Bank of China (PBOC) cut the benchmark 5 year loan prime rate by 0.15% and comments by Premier Li appear to indicate a speeding up in stimulus measures.

Source: Bloomberg, AMP

Australian economic events and implications

Wages growth disappoints again. Wages growth only edged up in the March quarter to 2.4%yoy. However, the average size of private sector pay rises for those who got an increase in the March quarter rose to 3.4%, which is the fastest since 2013. This suggests that faster wage rises are coming down the pipeline, which is consistent with the message from business surveys, anecdotes and the RBA’s business liaison.

And the tight and still tightening jobs market points to a pickup in wages growth ahead. Employment rose by a less than expected 4,000 in April and participation fell slightly. However, employment in prior months was revised up, full time jobs rose by 92,400, unemployment is now at 3.85% which is its lowest since 1974 and labour underemployment and underutilisation are at their lowest since 2008. The collapse in underutilisation points to stronger wages growth ahead.

Source: ABS, AMP

A further fall in unemployment is likely. Looking forward our Jobs Leading Indicator which is based on job openings points to continued strong employment growth. We continue to see unemployment falling to around or below 3.5% by year end.

Source: ABS, NAB, ANZ, AMP

What to watch over the next week?

In the US, the minutes from the Fed’s last meeting (Wednesday), at which it raised rates by 0.5%, are likely to be hawkish. On the data front, expect the composite PMI for May (Tuesday) to soften from the strong reading of 56 seen in April, new and pending home sales (due Tuesday and Thursday) are likely to fall, durable goods orders (Wednesday) are likely to rise again and personal spending for April (Friday) is likely to see a solid 0.6% gain. The core private final consumption deflator inflation (Friday) for April is likely to have fallen back to 4.9%yoy from 5.2%.

Eurozone business conditions PMIs for May (Tuesday) are likely to soften from the strong reading of 55.8 for the composite seen in April.

Japan’s composite PMI for May (Tuesday) is likely to show further improvement from April’s reading of 51.1 as reopening from the March quarter’s COVID restrictions continues.

The Reserve Bank of NZ (Wednesday) is expected to raise its cash rate again by 0.25%, taking it to 1.75%.

In Australia, the focus will likely be on the aftermath of the Federal election. On the data front, business conditions PMIs (Tuesday) are likely to remain strong, with the composite remaining around 56. March quarter construction data (Wednesday) is likely to show a 3.5% gain, business investment data for the March quarter (Thursday) is likely to rise 3%, with slight upgrades to business investment plans and April retail sales (Friday) are likely to show a 0.5% gain.

Outlook for investment markets

Shares are likely to see continued short term volatility as central banks continue to tighten to combat high inflation, the war in Ukraine continues and Chinese COVID lockdowns impact, driving fears of recession. However, we see shares providing reasonable returns on a 12-month horizon as global recovery ultimately continues, profit growth slows but remains solid and interest rates rise, but not to onerous levels, at least not for the next year.

Still-low yields and a capital loss from a further rise in yields are likely to result in ongoing negative returns from bonds.

Unlisted commercial property may see some weakness in retail and office returns (as online retail activity remains well above pre-COVID levels and office occupancy remains well below), but industrial property is likely to be strong. Unlisted infrastructure is expected to see solid returns.

Australian home price gains are likely to slow further, with average prices falling from mid-year as poor affordability, rising mortgage rates and rising listings impact. Expect a 10 to 15% top to bottom fall in prices over the next 18 months, but with a large variation between regions. Sydney and Melbourne prices are already falling.

Cash and bank deposits are likely to provide poor returns given the still low cash rate of just 0.25% at present, but they should improve as the RBA raises interest rates further.

The $A could fall further in the short-term if Chinese COVID lockdowns persist. However, a rising trend in the $A is likely over the next 12 months, helped by strong commodity prices, probably taking it to around $US0.80.

Dr Shane Oliver

Head of Investment Strategy and Economics and Chief Economist, AMP

(AMP Capital)