April 21, 2021

Dr Shane Oliver

Head of Investment Strategy and Economics and Chief Economist

(AMP Capital)

Whatever it is, the way you tell your story online can make all the difference.

Investment markets and key developments over the past week

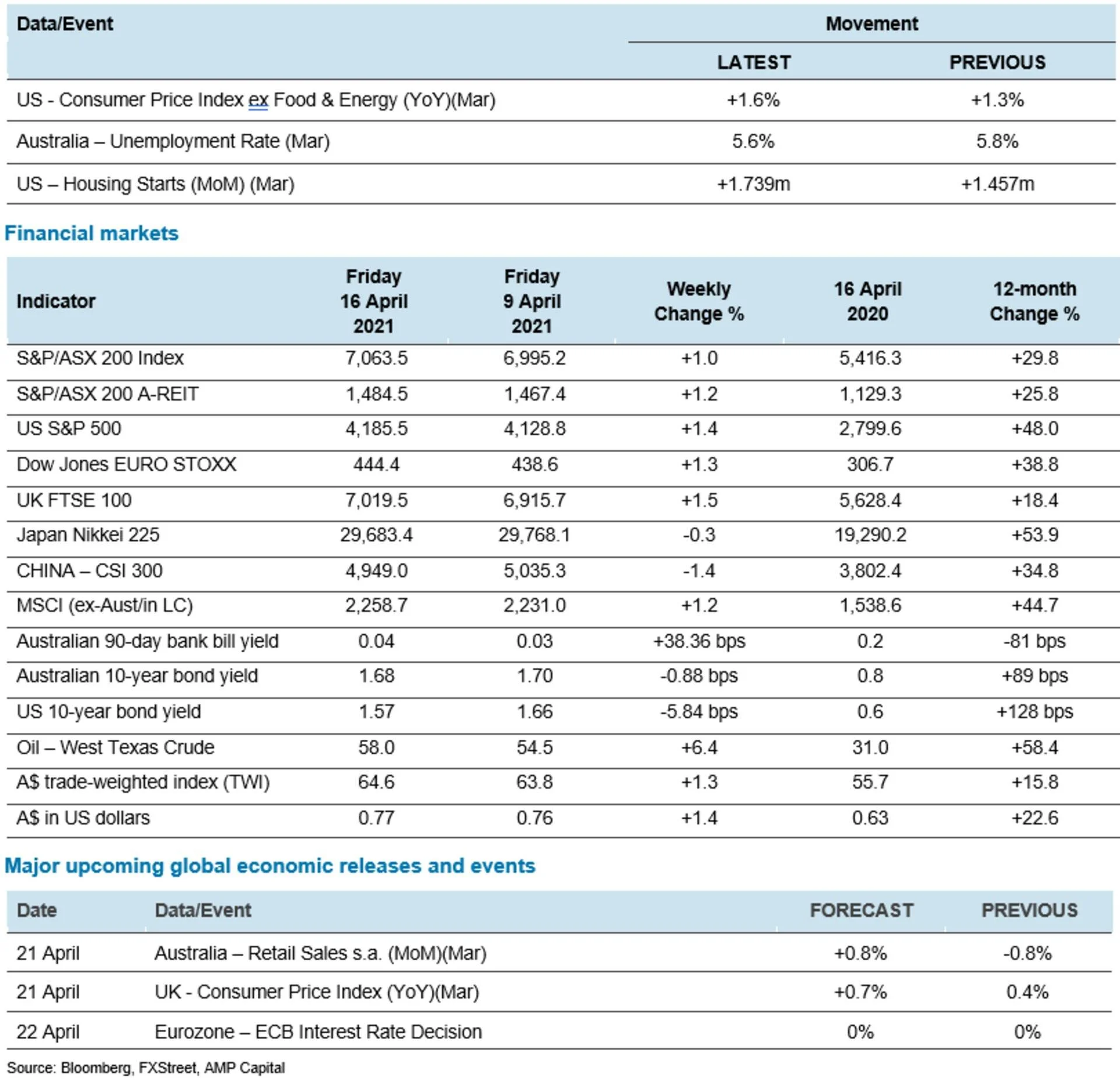

While Japanese shares fell -0.3% over the last week and Chinese shares lost -1.4%, US shares rose 1.4% to a new record high and European shares rose 1.3% to their highest since the year 2000, pushed by good economic data, a strong start to the US earnings reporting season, ongoing dovish comments from the US Federal Reserve (Fed) and tame bond yields. Reflecting the strong US lead, strong local data on confidence and jobs, and a bit of catch-up, Australian shares rose 1.0% to a new bull market high and are now just 1.4% away from an all-time high. The market was led higher by particularly strong gains in information technology (IT), health, material and retail stocks. Bond yields fell in the US and Australia, but rose slightly in Europe. Commodity prices and the A$ rose, which partly reflected a further decline in the US$.

Five reasons why bond yields have stabilised lately. The stabilisation in bond yields in recent weeks, despite more strong economic data and inflation readings, has been surprising for many. There are five reasons why they have stabilised:

coronavirus and vaccine related uncertainty has increased again;

central banks, led by the Fed, continue to reassure markets that the rise in inflation is likely to be transitory and they are not in a rush to validate the rise in bond yields with rate hikes;

bond investors had become very bearish, which is positive for bond prices from a contrarian perspective;

there have been no more surprise extra stimulus announcements lately; and

bonds had become technically oversold.

In other words, bond yields may have risen too far too fast earlier this year and were due a pause.

The recent stability in bond yields, when combined with optimism about reopening, good economic data, rising earnings expectations and dovish central banks enabled share markets to resume their rising trend, after a few wobbles earlier this year. Bond tantrums however are likely to return as economic recovery continues and central banks get closer to removing some stimulus. Coronavirus scares could also still cause volatility, but the rising bull market trend in shares is likely to remain on track. Our ASX 200 forecast for year-end remains 7,200, but this could be exceeded.

The trend in new global coronavirus cases and deaths remained up over the last week. New cases in the US have drifted up slightly, but they remain well down from recent highs. Europe has also fallen from its recent high. Japan and Canada however are trending up sharply and various emerging countries are seeing a renewed rapid increase including India, Turkey, Iran, Pakistan and various countries in South America. New coronavirus cases in Australia remain very low and have generally been due to returned travellers.

Whatever it is, the way you tell your story online can make all the difference.

Source: ourworldindata.org, AMP Capital

Whatever it is, the way you tell your story online can make all the difference.

Source: ourworldindata.org, AMP Capital

Vaccine rollout issues continue, with numerous uncertainties, but global recovery likely remains on track. Around 6% of the global population has now received one dose of vaccine, but this masks a huge divergence between developed countries (at around 37%) and emerging countries (at around 5%). Within developed countries, the UK is towards the front of the charge (at nearly 50%) and the US is at 38% (and running at over 3.5 million a day). Australia meanwhile is well behind, at around 5%. Europe is running at 17%, but appears to be speeding up, with Spain, Germany, France and Italy running around 1.5-2 million people per day each.

Whatever it is, the way you tell your story online can make all the difference.

Source: ourworldindata.org, AMP Capital

Apart from the ongoing resurgence in coronavirus cases globally, there has been more bad news on the vaccine/coronavirus front over the last week: the Johnson & Johnson (J&J) vaccine is being paused/investigated in the US and Europe following cases of rare blood clots, with it being a similar vaccine to that from AstraZeneca; a resurgence in cases in Chile leading to a renewed lockdown despite vaccinating 37% of the population highlights the risk in reopening before herd immunity has been reached (which holds lessons for the US and UK); vaccine uptake looks to be dropping off in the US South and Midwest, possibly not helped by the issues around the AstraZeneca and J&J vaccines adding to anti-vaxxer sentiment, running the risk of not reaching herd immunity and a pick-up in new cases – with similar issues in the UK; UK testing showed that coronavirus antibodies for first-vaccinated over 80 year olds have declined a bit (from 85% to 78% over three weeks), although second booster jabs should be longer lasting; and Pfizer has indicated that a third booster shot after a year and annual jabs may be necessary (although this is not really surprising).

There however has also been positive vaccine news: production of the Pfizer and Moderna vaccines is continuing to ramp up in the US and if, like the AstraZeneca vaccine, the J&J vaccine is only limited to over 50s, the issues regarding these vaccines are unlikely to be a huge problem for developed countries, albeit it could mean more significant delays in emerging countries; more results for the Moderna vaccine indicate that after six months it’s more than 90% effective and more than 95% effective in preventing severe cases, which is similar to results after six months for the Pfizer vaccine; 79% of 65 plus year olds in the US and a similar proportion in the UK have been vaccinated, so even if new cases rise again amongst the young, reopening can conceivably continue, as deaths and pressure on hospital systems should be minimal.

While the move away from the AstraZeneca vaccine in Australia will further slow the vaccine rollout and potentially push herd immunity to later this year (or early next year as we await the arrival of more Pfizer and Novavax vaccines), we remain of the view that the risk to the Australian recovery is small. Most of Australia has already reopened and has minimal restrictions, the economy has already recovered much faster than expected without vaccines and further local cases should be able to be minimized by inoculating returning travellers and all those associated with the hotel quarantine system. Vaccine delays in Australia and globally will likely impact the timing of the opening of international borders, but we had assumed it was at least a year away anyway and keeping Australians confined to Australia has been a net benefit for the economy, as international tourism is normally a net negative for Australia. That said, we may see more travel bubbles with select countries (like say Singapore) possibly on the proviso that the travellers are vaccinated.

Our Australian Economic Activity Tracker rebounded over the last week, with broad based gains after previous weeks which were impacted by the Brisbane lockdown. Our US Economic Activity Tracker rose slightly, but our European tracker fell again, not helped by ongoing lockdowns.

Whatever it is, the way you tell your story online can make all the difference.

Based on weekly data for eg job ads, restaurant bookings, confidence, mobility, credit & debt card transactions, retail foot traffic, hotel bookings. Source: AMP Capital

For some perverse reason I missed the release of Taylor Swift’s re-recorded 2008 album Fearless last week. Listening to it I reckon it’s better than the original. Given the way song licences work by re-recording each of her six initial albums she apparently has the ability to substantially destroy a big chunk of the value of the reported $300m Scooter Braun’s Ithaca Holdings (and its private equity backer) paid for Big Machine Records in 2019 that held the ownership rights to those albums. It highlights the importance of doing proper due diligence. Here is the old Love Story and new improved Love Story (Taylor’s Version). Change (Taylor’s version) is my favourite (for now). Gotta respect Taylor in all of this!

Major global economic events and implications

US economic data was strong. Retail sales surged in March on the back of reopening, recovery from storms and as 85% of adults received $1,400 stimulus checks. Sales by car dealers, sporting goods and hobby stores, online retailers and builder material and garden equipment stores are up 30% or more on pre coronavirus levels. Furthermore, small business optimism rose in March, regional manufacturing conditions indexes rose to very strong levels in April (pointing to a further recovery in industrial production), home builder conditions remained very strong, housing starts rose sharply in March (after bad weather depressed February figures), consumer sentiment rose and initial jobless claims plunged. Taken together, March and June quarter GDP growth could be pushing 10% annualised, but expect a second-half growth slowdown as the reopening/stimulus sugar-hit wears off.

However, the rebound in growth is now coming with a rebound in prices, with CPI inflation for March stronger than expected. The rise in inflation reflects a combination of base effects as last year’s price-falls drop out, a rebound in some prices due to reopening, higher commodity prices and goods supply bottlenecks. So far, underlying inflation measures such that the median CPI remain soft. In the absence of much stronger wages growth, the pickup in inflation should prove to be short lived – but it still has further to go yet, with headline CPI inflation likely to push to near 4% year-on-year in the next few months.

Meanwhile, Fed officials remain optimistic but dovish, with Fed Chair Powell confirming that the sequence of policy tightening would be to taper (or slow) bond purchases first, then hold the balance sheet steady, then hike rates – but all conditional on the Fed first making substantial progress towards its objectives and then with rate hikes actually meeting them.

Chinese March quarter GDP showed a massive 18.3% rise from the pandemic slump of a year ago, but this masked a slowing in quarterly growth to +0.6% quarter-on-quarter due to coronavirus restrictions early in the year and maybe some payback for upwardly-revised December quarter growth of 3.2% quarter-on-quarter. However, the pickup in most PMIs in March and stronger than expected retail sales and imports suggest that quarterly growth has probably accelerated again. March data for industrial production showed some loss of momentum in annual growth after the huge rebound for the year to January/February, but it remains strong and is likely to remain so, with strong domestic demand. Money supply and credit growth showed further moderation, but this likely reflects a renormalisation in monetary policy, as opposed to outright tightening. The slowdown in March quarter GDP growth will likely keep the authorities cautious in removing stimulus too quickly.

Australian economic events and implications

Australian data was strong. Consumer confidence rose in April to an 11-year high, business confidence remains strong and business conditions rose to their highest on record, all of which suggests that despite vaccine setbacks and snap lockdowns, the recovery remains on track and robust.

Whatever it is, the way you tell your story online can make all the difference.

Source: ABS, Melbourne Institute, AMP Capital

Surging jobs point to little impact from the end of JobKeeper, a slightly earlier than 2024 RBA rate hike and an even lower budget deficit. After a 70,700 surge in jobs in March, employment in Australia is now back above its pre coronavirus level, which is unequalled by most comparable countries. Unemployment has also fallen to 5.6%, which compares to its pre coronavirus level of 5.1%.

Whatever it is, the way you tell your story online can make all the difference.

Source: Bloomberg, AMP Capital

The continuing rebound in the jobs market adds to confidence that the ending of JobKeeper last month will have little impact. The number of people working fewer hours in March was only just above normal levels and those working zero hours was in line with normal levels, suggesting that the number of jobs actually vulnerable to being axed by the ending of JobKeeper is very low. Furthermore, record or near-record levels for job vacancies and business hiring plans pointing to continuing strong jobs growth ahead, suggesting that any laid off workers should be able to quickly find new jobs.

Whatever it is, the way you tell your story online can make all the difference.

Source: ABS, AMP Capital

Although the end of JobKeeper could see the unemployment rate flat line, or edge up slightly in the next few months, the continuing strength in our Jobs Leading Indicator points to unemployment falling to around 5% by year end.

Whatever it is, the way you tell your story online can make all the difference.

Source: ABS, Bloomberg, AMP Capital

While labour market utilisation (unemployment plus underemployment) at 13.5% is now just below its pre coronavirus level, non-accelerating inflation rate of unemployment (NAIRU), as it applies to the underutilisation rate, is probably around 10% or below, so we still have a way to go to get to full employment. This is consistent with the Melbourne Institute’s wages survey still pointing to very low wages growth. The strong jobs market suggests the conditions for a rate hike (wages growth greater than 3%) may fall into place earlier than the RBA is signalling, but this is probably still not till 2023, which remains our expectation for when the first-rate hike will occur.

Surging jobs mean surging personal tax revenue going to Canberra. Last month we revised down our 2020-21 budget deficit forecast to $150bn (from the Mid-Year Economic and Fiscal Outlook (MYEFO) that put it at $198bn), but the jobs surge means it could come in around $125bn, which will mean lower starting-point deficits in subsequent years as well. The starting point for the 2021-22 budget deficit could now be around $50bn.

What to watch over the next week?

In the US, expect to see April composite business conditions PMIs (Friday) remain very strong, around their March reading of 59.7 and March existing home sales (Thursday) and new home sales (Friday) to bounce back after storm-related falls in February.

The US March quarter earnings reporting season is already off to a good start with regard to bank results. This will ramp up in the week ahead, with the current consensus now being for a 28% rise in earnings per share (EPS) on a year ago – this has already been revised from +21% a week ago, but is likely to ultimately come in at around +35% to +40%.

The European Central Bank (ECB) (Thursday) is expected leave monetary policy on hold, but remain very dovish, with April business conditions PMIs (Friday) likely to be watched closely, after their surprise rise to a solid 53.2 in March despite coronavirus related setbacks.

Japanese core inflation for March (Friday) is likely to remain soft and business conditions PMIs for April will also be released on Friday.

In Australia, expect the minutes from the RBA’s last meeting (Tuesday) to remain dovish, preliminary March retail sales (Wednesday) to show a 1% bounce (after snap lockdowns in Victoria and WA weighed in February) and business conditions PMIs for April (Friday) to remain strong.Outlook for investment markets

Shares remain at risk of further volatility from a resumption of rising bond yields and coronavirus related setbacks. However looking through the inevitable short-term noise, the combination of improving global growth helped by more stimulus, vaccines and still-low interest rates augurs well for shares over the next 12 months.

Global shares are expected to return around 8% over the next year, but expect a rotation away from growth-heavy US shares to more cyclical markets in Europe, Japan and emerging countries.

Australian shares are likely to be relative outperformers helped by better virus control enabling a stronger recovery in the near term; stronger stimulus; sectors like resources, industrials and financials benefitting from the rebound in growth; and as investors continue to drive a search for yield (benefitting the share market as dividends are increased, resulting in a 5% grossed up dividend yield). Expect the ASX200 to end 2021 at a record high of around 7,200, although the risk is shifting to the upside.

Still ultra-low yields and a capital loss from rising bond yields are likely to result in negative returns from bonds over the next 12 months.

Unlisted commercial property and infrastructure are ultimately likely to benefit from a resumption of the search for yield, but the hit to space-demand and hence rents from the virus will continue to weigh on near-term returns.

Australian home prices are likely to rise another 15% or so over the next 18 months to 2 years, being boosted by record low mortgage rates, economic recovery and fear of missing out (“FOMO”), but expect a slowing in the pace of gains as government home buyer incentives are cut back, fixed mortgage rates rise, macroprudential tightening kicks in and immigration remains down relative to normal.

Cash and bank deposits are likely to provide very poor returns, given the ultra-low cash rate of just 0.1%.

Although the A$ is vulnerable to bouts of uncertainty and Reserve Bank of Australia (RBA) bond buying will keep it lower than otherwise, a rising trend is likely to remain over the next 12 months, helped by rising commodity prices and a cyclical decline in the US$, probably taking the A$ up to around $US0.85 by year-end.

Important notes

While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) (AMP Capital) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs.