April 1, 2021

Diana Mousina

Economist – Investment Strategy & Dynamic Markets

(AMP Capital)

Key points

The post-pandemic economic rebound is strong in Australia. But, after the initial bounce in activity, there is a need to reinvigorate the drivers of long-run economic growth. Productivity growth has been low in Australia and needs to lift to see a rise in incomes and living standards. Higher productivity growth is achieved through economic reform.

Areas in Australia that deserve policy attention include: lifting household incomes through labour market policies, improving education scores, improving incentives for business investment, reforming the taxation system and looking at the infrastructure pipeline.

Introduction

The focus for governments in 2020 and in 2021 is repairing the economy from COVID-19 and filling the economic growth hole left by the pandemic. This has been done by compensating or protecting household incomes from the hit to employment and supporting businesses through grants and loans. Economic issues that were pressing before the pandemic have largely been put on hold for now. But, once the economic recovery is more stable and vaccine rollout is well underway, there is a need to reinvigorate economic growth, which can be done with a combination of fiscal policy and reforms.

This Econosights looks at some structual issues that face Australia and options that the government could pursue to reboot the economy after activity has normalised post-pandemic.

Australia in context

The collapse in net migration is a hit to headline Australian GDP growth. Prior to COVID 19, Australia’s population was running at 1.5% per annum, with 65% of that growth coming from overseas migration (see the chart below).

Whatever it is, the way you tell your story online can make all the difference.

Source: ABS, AMP Capital

The government doesn’t expect net migration to get back to positive until 2022-23. Given the positive global vaccine rollout it may come sooner than that. But, it is unlikely that migration will quickly rise to its same pre-COVID levels within a short time frame.

The drivers of long-run GDP growth are labour productivity and the population. Higher population growth means higher GDP growth from a mathematical perspective. A larger population requires more spending on all components of “living” like housing, infrastructure and education. Australia has had high headline GDP growth compared to our global peers over recent years from the underlying boost from the population but once you account for population changes, GDP growth per capita (or per person) hasn’t outperformed as much (see chart below). Over the past decade, GDP growth per capita has averaged at 0.6% per annum in Australia, below the US at 1.0%, slightly higher than Japan at 0.5% and twice as high as Europe at 0.3%.

Whatever it is, the way you tell your story online can make all the difference.

Source: Bloomberg, ABS, AMP Capital

To lift GDP growth per capita, income growth needs to rise which can be done via higher productivity growth. Australia’s productivity growth (as measured by GDP per hour worked in the market sector) in the past decade averaged at 1.7% per annum. But, in recent years (before COVID-19), productivity growth was very low, averaging at less than 0.5% per annum. Productivity growth is achieved through long-term changes to the economy, usually through economic reform, rather than adjustments to fiscal and monetary policy.

Productivity growth can be harder to achieve in a services driven economy, like Australia (around 70% of GDP is from services activity), compared to manufacturing-intensive economies (usually in the emerging world). Some parts of services, like professional services and finance and insurance can often generate higher productivity growth as measured by traditional GDP measures, compared to other parts of services like health and education (although this doesn’t mean anything about the importance of that industry to the overall wellbeing of the economy which is difficult to measure by traditional GDP measures).

Areas to address in Australia

We highlight some areas in the Australian economy that require attention from policy makers.

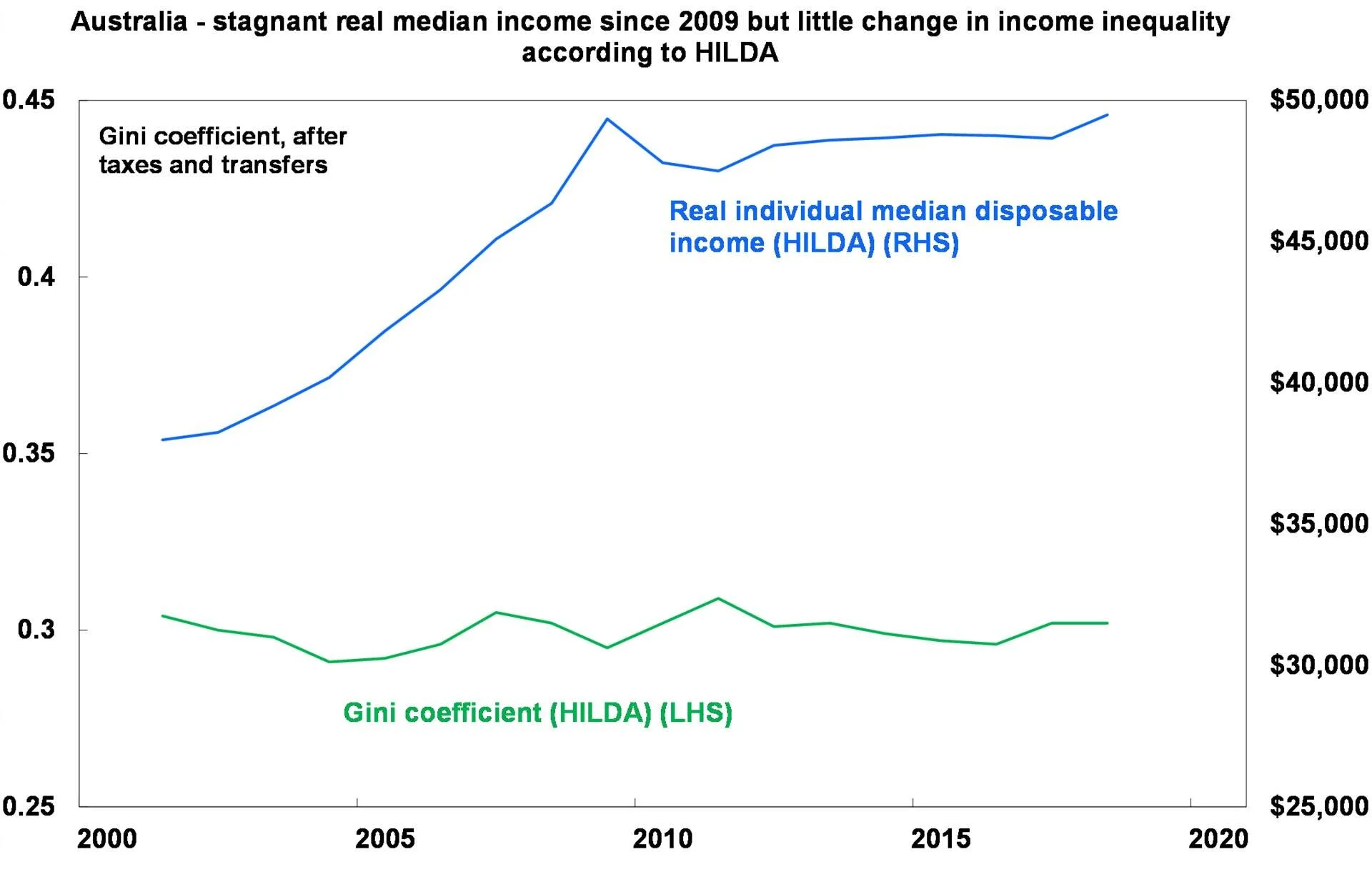

The labour market: Australian household median income growth has been stagnant since 2010 (see chart below) but inequality has not been rising in Australia (like it has been in other comparable countries like the US) according to the annual Household, Income and Labour Dynamics in Australia (HILDA) survey which tracks household indicators over time. Stagnant median income growth reflects the low wage environment that has been present in Australia since 2014. Wages growth rises as the labour market becomes “tighter” or as the unemployment rate moves closer to its potential or the “Non-Accelerating Inflation Rate of Unemployment” (NAIRU). The unemployment can never be zero because there will always be people moving between work. In Australia, the level of NAIRU is probably somewhere in the low 4’s orr even in the 3’s, which hasn’t been achieved since pre-Global Financial Crisis. Australia has also had a build up in “underemployment” which are those people that would like to work more hours. Underemployment (pre-pandemic) was averaging around 8.5% of the labour force compared to its historical average of around 6% which adds to downward wage pressures. So, employment growth needs to rise and underemployment needs to be reduced to get a lift in wages and household incomes.

While the Reserve Bank of Australia targets ‘full employment’ along with ‘price stability’ in the economy, expansionary fiscal policy is also helpful in assisting the labour market recovery and there is a case that the government (rather than just the Reserve Bank) should also be targeting full employment. The government’s recent “JobMaker” program aims at increasing the hiring of young people (aged 16-35) by giving businesses hiring credits for employing this age cohort. The program is expected to generate 450K jobs or ~3% of employment over 2 ½ years. So far, the scheme has been off to a slow start historically the use of hiring credits use in Australia has shown they arent too effective in lifting rates of hiring.

Inequality measures in Australia have not been deteriorating over the past 20 years. The Gini coeffecient (a common measure of inquality which looks at the distribution of income amongst a population with 0 being perfect equality and 1 being perfect inequality) has remained relatively steady in Australia over the 18 years of the HILDA survey (see chart below).

Whatever it is, the way you tell your story online can make all the difference.

Source: HILDA, AMP Capital

Middle-income jobs are at risk in Australia (and across many other developed countries) in the longer run from technological changes, and routine manual and cognitive jobs are already declining as a share of the labour force (see chart below).

Whatever it is, the way you tell your story online can make all the difference.

Source: ABS, RBA, AMP Capital

The role for governments around managing the impact of technology on employment includes access to high-quality education and training programs, appropriate school and university curriculum’s and ensuring funding is targeted towards areas with a low risk of automation.

Another current issue is around skills shortages building up post pandemic. Many Australian businesses are currently talking about the need to bring back overseas migration because of skills shortages in areas like hospitality and construction. But, the lack of current overseas migration seems like a good opportunity to reduce the unemployment rate by bringing domestic workers into those industries with skills shortages via re-training initatives.

Education: Education levels appear to be slipping. The OECD run a survey every three years of 15-year old students reading, maths and sceince knowledge known as the Programme for International Student Assessment (PISA). In 2018, reading scores were above the OECD average and maths and science were in line with the average. However, Australia’s scores on reading have been declining since 2000 (the first available reading), mathematics scores falling since 2003 and science since 2012. The latest major reform to education were the “Gonski” changes to school funding in 2012. With testing scores falling for years, changes to curriculum are required to lift performance which is more of an issue for the State governments who are responsible for education.

Business incentives: Australian business investment has been subdued since mining investment peaked in 2012 (see chart below).

Whatever it is, the way you tell your story online can make all the difference.

Source: ABS, AMP Capital

It was expected that non-mining investment would pick up at the time that mining investment was declining. But, non-mining business investment has been stable at ~5% of GDP over the past 8 years and is not showing any signs of rising, despite the low rate environment.

Higher business investment drives rises in productivity growth. But, simply having a low interest rate environment and encouraging businesses to adopt lower project hurdle rates (which the Reserve Bank has been pushing for some time) is unlikely to generate higher investment growth. Business investment requires certainty about the economic, political and regulatory outlook. According to the quarterly NAB business survey, the top three most influential issues affecting business confidence are demand, state government policies/regulation and federal government policies. Interest rates rank towards the bottom of the list at 15th place (out of 20). Other areas that businesses often cite as problematic include: heavy industry regulation because it delays decisions, outdated state tax systems and complex enterprise bargaining agreements. Some clarity around the future energy policy in Australia would also be positive. Government support for innovation and support for research is also important as technology is becoming more critial to all business operations.

The Federal government’s latest temporary business tax incentives in the 2020 budget (that allow full depreciation of assets and allowance of losses to be offset against profits) should be a short-term positive for near-term machinery and equipment investment, but it is yet to show up in a large extent in expected capital spending plans. Some assets are excluded from the temporary tax incentives, including assets used in research and development costs and large capital works like buildings and structural improvements.

Taxation: There has been talk of a broad review into the Australian tax system for years. The latest major change to taxation has been NSW’s proposal to reform stamp duty (from an initial lump sum payment when purchasing a property to an annual property tax) which would help to alleviate affordability pressures of entering the housing market. Other states and territorities should consider a similar system. Other taxes that need to be looked at is the Goods and Services Tax (GST). A broadening of goods and services covered by the GST should be investigated, as over time it has tended to cover a smaller share of household spending. This could be met with some personal tax cuts (which Australia has a very high reliance on) and redistributions to low-middle income households. Payroll taxes are also another candidate for reform because they are levied at different rates by the states which creates distortions in the tax system.

Infrastructure: While government infrastructure spending is not a reform item, it is an important part of government spending. Spending on transport infrastructure has been booming over recent years and the value of government infrastructure projects has cotninued to grow (see chart below).

Whatever it is, the way you tell your story online can make all the difference.

Source: ABS, State and Federal Budgets, AMP Capital

Some clarity on future infrastructure plans and priorities would support business investment as per a priority list. Infrastructure Australia (an independent infrastructure advisor) has a “priority list” of projects it releases which details the key areas it deems as necessary of improvements which can be used as a starting point.

Implications

A focus on lifting productivity growth is important for long-run economic growth in Australia. The current reliance on monetary and fiscal policy to support GDP growth makese sense for the “pandemic period” Australia is still operating in. But, after the health crisis is worked through, policy makers will need to address the structual issues that face Australia’s economy in the long-run.