By now you have all probably seen the news on the spike in reported cases outside of China. The coronavirus disease is apparently communicable even by those who are not showing signs of having it, which is making it harder to control. The number of new infections in Wuhan/Hubei and the rest of China are falling sharply (latest new infection rate was 630 in Hubei and 20 in the rest of China). However, markets are reacting to the jump in reported cases cumulative outside China (mostly in S. Korea, Italy, Japan and Iran), as well to the 700 people infected on the Diamond Princess ship (out of 3700 total crew/passengers).

Here is the latest information from the Chinese Center for Disease Control on mortality rates. While the average coronavirus mortality rate is reported to be around 2.3%, COVID-19 primarily affects older individuals with pre-existing conditions, whose mortality rates are much higher. Individuals below the age of 50 and/or those with no pre-existing conditions have mortality rates well below 2% (almost 0% for people below the age of 40). Be careful with mortality rates, there are a lot of them being reported, and they all depend on the methodology. For example, as a percentage of hospitalized cases with a specific outcome (mortality or discharged/recovered), mortality rates are closer to 10%. And out of all cases of currently infected individuals, 78% are in mild condition and 22% are in critical condition.

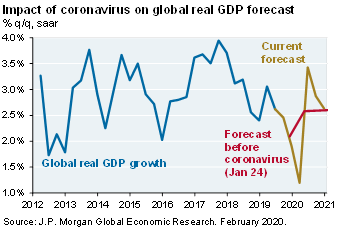

It is hard to pinpoint what the economic outcomes might be, but they look worse than they did a few weeks ago. The first chart below is an estimate of the impact of the virus on Q1 GDP in different countries. The second chart looks at “supplier delivery times”, which reflects the extent to which supply chains are disrupted by the virus. The last time the disruption rate was this high was in the wake of the Fukushima tsunami/earthquake.

Within China, we are tracking indicators that reflect the impact of the lockdown on Chinese activity. Here’s how to read the next chart. Twenty days after the Chinese Lunar New Year (Feb 14) was the low point for economic activity due to quarantines and travel bans. At that time, for example, electricity consumption was running at 40% of its normal level for that time of the year. As of the latest reading, that hasn’t changed. Only coal deliveries, passenger flows and home sales have picked up since the low levels, and even these have only risen by a small amount. I think it’s fair to say that this is the biggest negative shock the global economy has seen since the financial crisis. It’s hard to know for sure, but the decline in the US freight index could reflect part of the knock-on effects of the situation in China.

Even so, JP Morgan’s Investment Bank, as well as a lot of other research providers we follow, believe that there will be an eventual bounce once the crisis is over (second chart), and that global growth will revert to where it was before the virus outbreak. This has been the pattern after other viruses, and after natural disasters such as the Kobe earthquake and the Fukushima tsunami.