Dr Shane Oliver

Head of Investment Strategy and Economics and Chief Economist

(AMP Capital)

Key points

The coronavirus outbreak is just another of a long list of worries. Our natural inclination to zoom in on negative news combined with a massive ramp-up in the availability of information is arguably making us worse investors: more fearful, more jittery, more short-term.

Five ways to help manage the noise and turn down the worry list are: put the latest worry in context; recognise that shares return more than cash in the long-term because they can lose money in the short-term; find a process to help filter noise; make a conscious effort not to check your investments so much; look for opportunities that investor worries throw up.

Introduction

2020 has seen a very noisy start to the year with one major event with significant human and investment market implications after another. For Australia it started with an intensification of the bushfires but moved on to a significant ramping up of US/Iran tensions where, according to President Trump, war came “closer than you thought” and now the coronavirus outbreak is creating fears of a global pandemic and a big hit to global economic activity. These are scary in terms of their human consequences, but also in terms of the potential economic fallout and what it means for investors. The coronavirus outbreak in particular continues to pose significant uncertainty around the short-term economic outlook. In terms of the key things to watch there is some good news with signs of a reported slowing in new cases in China and still limited transmission outside China (which has 99% of cases).

Source: PRC National Health Commission, Bloomberg, AMP Capital

And the mortality rate at just over 2% remains lower than with SARS. Against this there remains much debate about the true number of cases, it’s common in outbreaks to see periods of stabilisation only to be followed by a spike in cases and the disruption to economic activity in China and from global travel bans remain significant all of which makes it easy to imagine the worst in terms of economic consequences. Each week China remains say 2/3rds shut it knocks 1.3% off its GDP or 0.25% directly off global GDP.

Then again much of 2018 and 2019 saw endless talk about how much the trade war was going to knock off global growth. More fundamentally, the coronavirus outbreak is part of a seemingly never-ending worry list which is receiving an ever-higher prominence as the information age enables the rapid dissemination of news, opinion and noise. But as Frank Zappa warned “information is not knowledge, knowledge is not wisdom”. The danger is that information overload is making us worse investors as we focus on one worry after another resulting in ever shorter investment horizons.

Are the worries more worrying than ever?

When I was a teenager in the 1970s I used to bemoan my grandmother for reading too much gloom into the nightly TV news and telling me that the world is much worse today than when she was young….when there was WW1, Spanish influenza that reportedly killed around 50 million people, the Great Depression and WW2 when her brother was killed. However, now it seems the worry list is even bigger. Yes, there is a fundamental element as global growth is slower, technological disruption is leading to worker anxiety and inflated expectations, and the world seems awash in geopolitical risks.

But there is a huge psychological aspect to this that is combining with the increasing availability of information and intensifying competition amongst various forms of media for clicks, that is magnifying perceptions around various worries.

We all suffer from a behavioural trait that in its financial manifestation is known as “loss aversion” in that a loss in financial wealth is felt much more distastefully than the beneficial impact of the same sized gain. This probably reflects the evolution of the human brain in the Pleistocene age when the trick was to avoid being eaten by a sabre-toothed tiger or squashed by a woolly mammoth. This makes us biased to be more risk averse and on the lookout for threats which leaves us more predisposed to bad news stories as opposed to good news stories. So bad news and gloom find a more ready market than good news or balanced commentary as it appeals to our instinct to look for threats. Hence “bad new sells”. Of course, this has always been the case so there is nothing new here.

The big change though is that we are now exposed to more information in relation to everything including our investments. This is great in the sense that we can check things, analyse them and sound informed easier than ever. But often we have no way of weighing such information and no time to do so. If we can’t filter it, it becomes information overload and noise. This can be bad for investors as when faced with more (and often bad) news we can freeze up and make the wrong decisions with our investment as our natural “loss aversion” combines with what is called the “recency bias” that sees people give more weight to recent events which can see investors project recent bad news into the future and so sell after a fall.

Finally, the problem is being compounded by an explosion in media outlets all competing for your attention. We are now bombarded with economic and financial news and opinions with 24/7 coverage by web sites, subscription services, finance updates, dedicated TV and online channels, etc. And in competing for your attention, bad news and gloom trumps good news and balanced commentary as “bad news sells.”

So naturally it seems that the bad news is ‘badder’ and the worries more worrying than ever. Google the words “the coming financial crisis” and you get 236 million search results – up from 115 million when I did it 18 months ago – with titles such as:

“World economy is sleepwalking into a new financial crisis”;

“4 early warnings signs of the next financial crisis”;

“The coming economic crash”;

“Why the next global financial crisis may dwarf…2008”; and

“Financial crisis – Bible prophecy & current events.”

The trouble is that there is no evidence that all this noise is making us better investors. Average returns are no higher than in the past. A concern is that the combination of a massive ramp up in information combined with our natural inclination to zoom in on negative news is making us worse investors: more fearful, more jittery and more short term focussed.

Five ways to manage the perpetual worry list

So here we take another look at five ways to manage the worry list and turn down the noise:

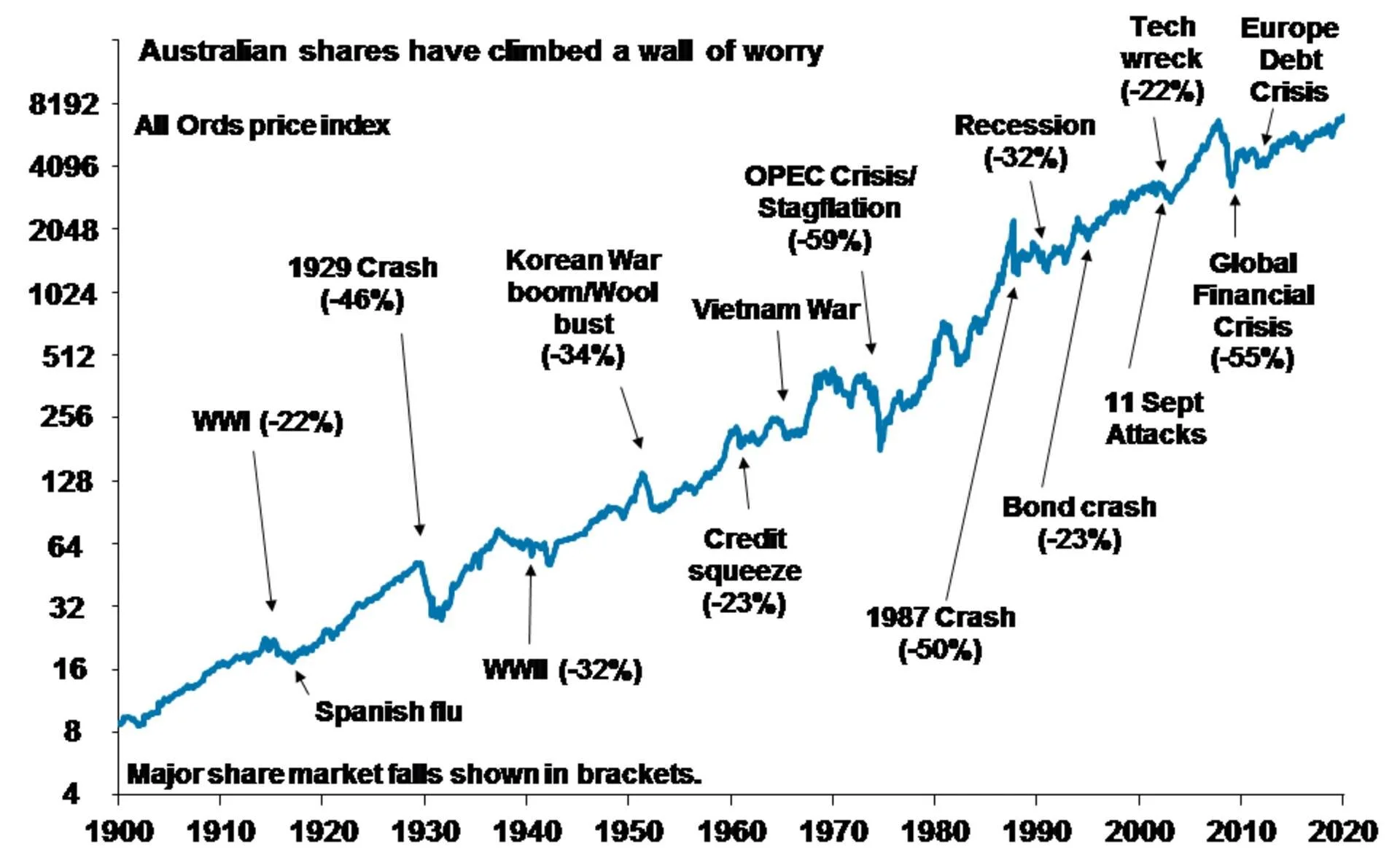

Firstly, put the latest worry list in context. Remember that there has always been an endless stream of worries. Here’s a list of the worries of the last five years that have weighed on markets at various points: deflation; commodity/oil crash; Grexit; China worries; Brazil and Russia in recession; manufacturing slump globally; Fed rate hikes; Brexit; South China Sea tensions; Trump; Eurozone elections; North Korea; Germany; Catalonia; Italy; US inflation and rates; Trade war; China slowdown; Aust Royal Commission; Aust housing downturn; US government shutdown; inverted yield curves; impeachment; Aust recession fears; and Iran tensions. Yet despite this extensive worry list investment returns have actually been okay with average balanced growth super funds returning 7.3% pa over the last five years after taxes and fees. In fact, the global economy has had plenty of worries over the last century, but it got over them with Australian shares returning 11.8% pa since 1900 and US shares 9.9%pa.

Source: ASX, AMP Capital

And while history doesn’t repeat it does rhyme and it’s often useful to look back at previous similar events to the latest worry to see how they panned out. This is where the experience around SARS is useful in relation to the latest coronavirus outbreak.

Secondly, recognise how markets work. A diverse portfolio of shares returns more than bonds and cash over the long-term because it can lose money in the short-term. While the share market is highly volatile in the short-term it has seen strong returns over rolling 20-year periods. So, volatility driven by worries and bad news is normal. It’s the price investors pay for higher long-term returns.

Source: Global Financial Data, AMP Capital

Thirdly, find a way to filter news so that it doesn’t distort your investment decisions. For example, this could involve building your own investment process or choosing 1-3 good investment subscription services and relying on them. Or simpler still, agreeing to a long-term strategy with a financial planner and sticking to it. Ultimately it all depends on how much you want to be involved in managing your investments.

Fourthly, don’t check your investments so much. If you track the daily movements in the Australian All Ords price index or the US S&P 500, it has been down almost as much as it has been up. So, day to day it’s pretty much a coin toss as to whether you will get good news or bad. By contrast if you only look at how the share market has gone each month and allow for dividends the historical experience tells us you will only get bad news 35% of the time. Looking only on a calendar year basis, data back to 1900 indicates that the probability of bad news in the form of a loss slides further to 20% for Australian shares and 27% for US shares. And if you can stretch it out to once a decade positive returns have been seen 100% of the time for Australian shares and 82% of the time for US shares.

Data from 1995 and 1900. Source: Global Financial Data, AMP Capital

The less frequently you look the less you will be disappointed and so the lower the chance that a bout of “loss aversion” triggered by a bad news event will lead you to sell at the wrong time. So, try to avoid looking at market updates so regularly.

Finally, look for opportunities that bad news throws up. Periods of share market turbulence after bad news throw up opportunities as such periods push shares into cheap territory.

Concluding comment

My long-term experience around investing tells me that it’s far more productive to lean into prognostications of financial gloom because most of the time they are wrong and end up just distracting investors from their goals.

Important notes

While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) (AMP Capital) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent of AMP Capital.