December 16, 2020

Dr Shane Oliver

Head of Investment Strategy and Economics and Chief Economist

(AMP Capital)

Investment markets and key developments over the past week

Global share markets had a pull back over the last week with the absence of a new stimulus deal and rising new coronavirus cases in the US weighing. For the week US shares fell 1%, Eurozone shares fell 1.3%, Japanese shares lost 0.4% and Chinese shares fell 3.5%. Despite this, Australian shares rose for the sixth week in a row, albeit it was only a small gain of 0.1%, with a surge in the iron ore price and higher oil prices pushing up resource stocks along with good gains in IT and consumer discretionary stocks offsetting weakness in property, industrial and retail shares. Bond yields fell but oil, metal and iron ore prices rose. The surge in commodity prices, notably iron ore, helped push the A$ above US$0.75 to its highest since first half 2018.

Shares remain stretched and at risk of a correction after their strong run since early November. However, beyond short term noise more upside is likely as momentum is very strong, the Santa Claus seasonal rally normally gets underway from mid-December and investors are yet to fully discount the potential for a very strong economic and profit recovery next year as stimulus combines with vaccines. Cyclical recovery shares like resources, industrials and financials are likely to be relative outperformers as the focus shifts from pandemic to recovery, and this should benefit the Australian share market over US shares. The A$ is likely to continue to head higher towards our forecast of US$0.80 by end next year on the back of rising commodity prices and a falling US dollar. The RBA may ultimately increase and extend its quantitative easing program to try and combat this – but this will likely only be able to slow the A$’s ascent as opposed to stopping it.

After a brief stabilisation, the trend in new global coronavirus cases is rising again. While new cases in Europe are well down from recent highs it looks to have stopped falling and after a brief pause around Thanksgiving new cases in the US are surging higher again in all regions. Thanksgiving itself looks to have been a super spreader event and Christmas runs the risk of being the same. In other major developed countries, there are signs that Japan’s third wave may be peaking but Canada is still seeing a rapid rise in new cases (currently running just below 7000 a day), Brazil has seen a resurgence in new cases back to its July high but new cases are continuing to trend down in India.

Source: ourworldindata.org, AMP Capital

While measured fatality rates are well down from their highs across developed countries – reflecting much more testing picking up more cases and better treatments – the reality is that deaths in the US have now surpassed their April high and the growth in hospitalisations is overwhelming medical systems in certain areas. This in turn is what drove the recent lockdowns in Europe and is now driving more regional lockdowns in the US (eg, in California).

Source: ourworldindata.org

Vaccines are on the way – with the UK, Canada, Saudi Arabia, the US and Mexico approving Pfizer’s vaccine and starting to roll it out. Interestingly results show it may be 98-99% effective after the first 7-14 days (as it takes time for the immune response to kick in). The apparent failure of the University of Queensland’s vaccine is disappointing, but Australia has invested in a range of different vaccines. There is still a long way to go though and even with more vaccine approvals they won’t deal with the current waves in many countries but will help significantly from second half next year with a good chance of reaching herd immunity globally by the end of 2021 or early 2022. This is continuing to help share markets look through the current problems with the virus and its economic impact.

Australia is continuing to report a low level of new covid cases – essentially just returned travellers. The graph is so boring I won’t bother with it this week, but fingers crossed it remains that way. Meanwhile, Australia’s relative performance in terms of dealing with coronavirus – measured across per capita new cases, total cases, deaths and testing – continues to stack up very well. In fact, we are ranked at number 1 in the OECD. If we had the same experience with deaths per capita as the US we would have now lost 22,500 people to it, compared to 908 – that’s an extra 21,600 people saved.

OECD countries ranked in terms of controlling coronavirus

Source: covid19data.com.au; AMP Capital

Our weekly Economic Activity Trackers remain divergent. In Europe they have continued to move up from their lows and are likely to improve more significantly in the next month or two if lockdowns are eased, but they still point to a significant contraction in December quarter GDP. Our US tracker was flat over the last week but is still in a downtrend in response to increasing lockdowns pointing to slowing economic conditions.

Based on weekly data for eg job ads, restaurant bookings, confidence, mobility, credit & debt card transactions, retail foot traffic, hotel bookings. Source: AMP Capital

By contrast our Australian Economic Activity Tracker has moved up further and has now recovered to year ago levels with a broad-based improvement across confidence, restaurant and hotel bookings, spending, traffic, job ads and mobility. This is consistent with the good control of coronavirus seen in Australia and the reopening of the economy – notably in Victoria. This all suggests that Australia will see a continuing solid economic recovery this quarter, while the US may be slower, and Europe will see a contraction. All things being equal this is relatively positive for the Australian share market and the A$.

Time is just about up on President Trump’s attempts to overturn the election. While Mr Trump now seems to think he won because he got more votes than the 63 million he did in 2016, the reality is that Joe Biden was also in the election and got many more again (with 81.2 million votes versus Trump’s 74.2 million). The Trump campaign and associates have lost or dropped more than 50 lawsuits designed to reverse the result in Trump’s favour with most notably the US Supreme Court denying an application to overturn the result in Pennsylvania and rejecting a bid from Texas – that Trump called “the big one” – asking it to overturn the results in Pennsylvania, Michigan, Wisconsin and Georgia. So, the electoral college is almost certain to have voted by Monday’s deadline with 306 votes to 232 in favour of Biden (or close to it as there are sometimes some “faithless” voters). Trump has said that if the electoral college confirms that Biden has won then he will leave the White House. Of course, he can continue to claim he won and will remain President up until January 20 so could still cause a bit of havoc along the way. Meanwhile polling for the two Senate seat elections in Georgia is tight with the Democrats just ahead on some polls, although the odds of the Democrats winning both and hence Senate control remains less than 50%.

Although there has been progress towards a new stimulus package in the US worth around $900bn sticking points remain around aid for states and protections for businesses from Coronavirus related lawsuits. At this stage the odds of a deal before Christmas are only just above 50%. Meanwhile a one week stop gap funding bill has been passed avoiding a Government shutdown after December 11, but a longer-term bill will need to be passed in the week ahead to avert a shutdown after December 18 and this appears likely as it’s hard to see either side of politics wanting to see another shutdown now.

Brexit talks…is that still a thing? – yep even though its more than 4 years after the 2016 referendum…regarding the future trading relationship between the EU and UK are on a knife edge with time rapidly running out. Fishing rights, the governance of the deal and fair competition rules remain key differences. The fair competition rules appear to be a big sticking point with the UK seeing it as an issue over sovereignty. UK PM Johnson has warned Britain to prepare for “something like an Australian relationship with the EU” – but that relationship is not so good with numerous barriers to Australian exports. If a deal is not reached then the UK will have the much talked about hard Brexit at year end resulting in the imposition of tariffs, quotas and additional costs in trade between the two which would be far more negative for the UK as 43% of its exports go to the EU whereas less than 10% of EU exports go the UK.

Only two weeks to Christmas. It’s bleak looking in Europe, the US and other parts of the world with covid raging but at least things are feeling a lot better this year in Australia coming into Christmas without all the smoke and bushfires and far better virus control. Five years ago Kylie Minogue put out a neat Christmas album – my favourites were White December and 100 Degrees (with Dannii Minogue).

Major global economic events and implications

US data was mixed with a rise in job openings, only a slight fall in small business optimism which is still strong, a fall in continuing jobless claims but a sharp rise in initial jobless claims suggesting which may be a further sign that the jobs market is slowing. Meanwhile, core consumer price inflation was a bit higher than expected at 1.6% year on year although the upside surprise looks temporary.

To deal with renewed economic weakness the ECB extended its pandemic quantitative easing program by another €500bn out to at least March 2022 (but with the monthly amount varying to maintain favourable financial conditions) and it extended its -1% conditional cheap bank funding program by 12 months. It means ongoing massive easing but the ECB under Lagarde still seems to be lagging the “whatever it takes” approach of Draghi and may have to be more aggressive given a likely further rise in the Euro.

Japanese data was mixed with a solid rise in machine orders and stronger household spending but a fall in business and household confidence.

Chinese data saw surprising strength in exports particularly to the US and strong credit growth which is consistent with continued solid growth. Meanwhile, food prices pushed CPI inflation negative but with core inflation remaining weak and producer deflation abating slightly.

Australian economic events and implications

Australian economic data was yet again very strong with further improvements in business conditions and confidence according to the NAB business survey, a rise in the Westpac/MI measure of consumer confidence to its highest in ten years and a further recovery in ANZ job ads. This is all consistent with the message from our Australian Economic Activity Tracker referred to earlier which has been pointing to a continued solid recovery in Australia.

Source: Westpac/MI, AMP Capital

While the Westpac/MI survey showed little enthusiasm for property, real estate and shares as the “wisest place for saving” it did show reduced interest in bank deposits and paying debt and increased interest in spending.

Source: Westpac/MI, AMP Capital

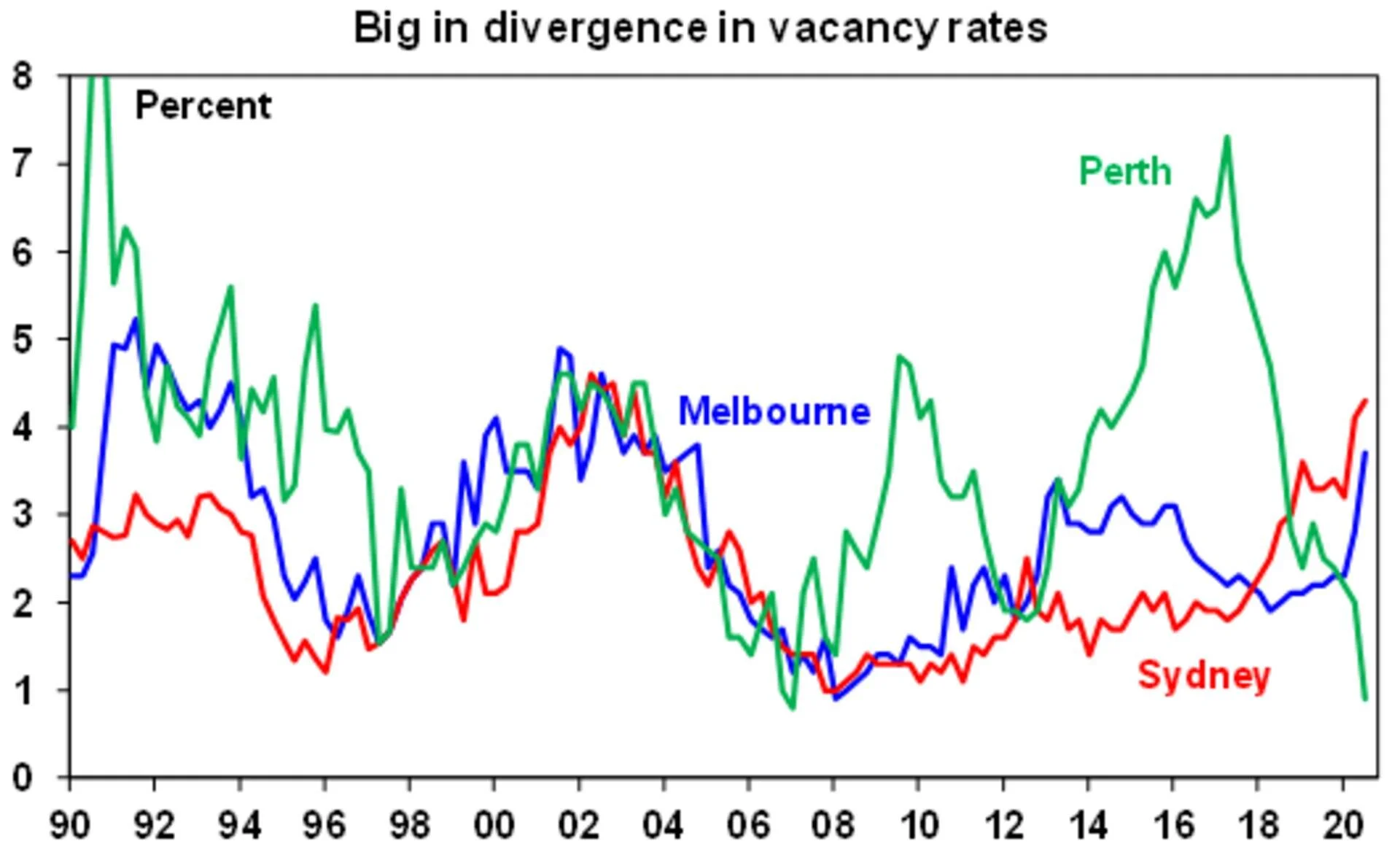

The divergence in residential vacancy rates across Australia is interesting. Basically: Perth and Darwin are seeing a collapse in their vacancy rates; Brisbane, Adelaide, Canberra and Hobart all have low and falling vacancy rates; but they have spiked higher in Sydney and Melbourne. Several factors are at play including the “escape from the city” phenomenon thanks to covid and working at home and the hit to immigration and foreign students hitting Sydney and Melbourne far worse than other cities at a time when they have just seen unit building booms. It’s likely to put more downwards pressure on rents and prices on inner city units in those two cities. A similar phenomenon is being seen in Manhattan which is seeing unit rents fall back to levels last seen 10 years ago.

Source: REIA, AMP Capital

While NSW and Victoria lost their AAA credit ratings from Standard & Poors its unlikely to have much impact on borrowing costs, particularly for NSW. Budget outlooks are likely to improve from here, yield moves following rating moves often go either way and RBA bond buying, including of state government bonds, continues.

The appetite for Australia government debt was highlighted by the sale of 3-month Treasury Notes at a slight negative yield. While this looks irrational with the RBA saying its “extraordinarily unlikely” to take the cash rate negative, Australian yields may still be seen as attractive for some foreign investors where negative yields are the norm and this demand could quite easily dip them negative at times given that the cash rate and the three year bond yield target at 0.1% are only just above zero.

What to watch over the next week?

In the US, the focus will be on the Fed (Wednesday) which is expected to provide more dovish guidance around its quantitative easing program. On the data front, expect somewhat softer readings for December New York and Philadelphia regional manufacturing indexes (due Tuesday and Thursday) along with business conditions PMIs (Wednesday) due to increasing lockdowns, a modest rise in industrial production (also Tuesday), a slight fall in November headline retail sales due to lower auto sales and a still very strong NAHB homebuilder conditions index (both Wednesday) but still strong housing starts (Thursday).

Eurozone business conditions PMIs (Wednesday) are likely to stabilise after recent sharp falls.

The Bank of England (Thursday) is likely to expand its QE program and remain dovish.

In Japan, the Tankan business conditions survey for the December quarter (Monday) is likely to show an improvement, the December business conditions PMI will be released Wednesday and CPI data for December (Friday) is likely to show ongoing deflation. The Bank of Japan (Friday) is expected to leave monetary policy on hold and remain dovish.

Chinese economic activity data (Tuesday) is expected to show a further acceleration in the rate of growth in industrial production, retail sales and investment.

In Australia, the Federal Government’s Mid-Year Economic and Fiscal Outlook which is due to be released in the week ahead is likely to see an upgrade to the growth outlook and a downgrade to the budget deficit projections reflecting stronger revenue flows and slightly less emergency spending than expected in the Budget. Expect 2020-21 GDP growth to be revised up to flat from -1.5%, unemployment at June 2021 to be revised down to 7% from 7.25% and the 2020-21 budget deficit to be revised down to a still huge $200bn from $214bn. Hopefully peak deficit has been seen, but peak debt will be years away.

Meanwhile, the minutes from the RBA’s last board meeting (Tuesday) are likely to remain dovish with the RBA prepared to do more bond buying if needed. On the data front, jobs data (Thursday) is expected to show flat employment after last month’s surprise179,000 surge and unemployment remaining at 7% and business conditions PMIs (Wednesday) are likely to show a further improvement. Weekly payroll jobs data will also be released on Tuesday.

Outlook for investment markets

Shares could see a short term pause after recent strong gains. But we are now into a seasonally strong period of the year for shares (particularly from mid-December) and on a 6 to 12-month view shares are expected to see good total returns on the back of ultra-low interest rates and a strong pick-up in economic activity helped by stimulus and likely vaccines.

Low starting point yields are likely to result in low returns from bonds as the dust settles from coronavirus.

Unlisted commercial property and infrastructure are ultimately likely to benefit from a resumption of the search for yield but the hit to economic activity and hence rents from the virus will weigh heavily on near term returns.

Australian home prices are being boosted by ever lower interest rates, government home buyer incentives, income support measures and bank payment holidays but high unemployment, a stop to immigration and weak rental markets will likely weigh on inner city areas and units in Melbourne and Sydney into next year. Outer suburbs, houses, smaller cities and regional areas are in much better shape and will see stronger gains in 2021.

Cash and bank deposits are likely to provide very poor returns, given the ultra-low cash rate of just 0.1%.

Although the A$ is vulnerable to bouts of uncertainty about coronavirus, the economic recovery and China tensions and RBA bond buying will keep it lower than otherwise, a continuing rising trend is likely to around US$0.80 over the next 12 months helped by rising commodity prices and a cyclical decline in the US dollar.

Important notes

While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) (AMP Capital) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent of AMP Capital.

This article is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.