Weekly market update – Investment markets and key developments

Concerns about the banking system have eased this week but have not been completely erased. Expectations for fewer central bank interest rate hikes (because of the risks in the banking system and the tightening in lending standards which will weigh on economic growth and is a de facto monetary tightening) is helping to lift shares, with the US up 3.5% this week, Australia +3.2%, Eurozone +4.5%, Japan +2.4% and China +0.6%. Bond yields rose over the week on fewer banking sector issues, commodity prices were also mostly higher with oil back up to nearly $80/barrel after declining down to $72 in recent weeks. The $A was up slightly to 0.668USD.

Policymakers are still attempting to control risks from the banking sector with news this week that the Fed’s emergency lending program could be expanded which would help regional banks like First Republic Bank (that has been caught up in the recent crisis), the announcement that First Citizens bank would buy all the deposits and loans of Silicon Valley Bank and expectations for more regulation for mid-sized banks (including lifting liquidity requirements and enhanced stress-testing). However, there are still pockets of concern (news articles this week mentioned Charles Schwab bank as the next domino to fall) so it’s too early to say that financial contagion risks have been fully contained. There was no further decision from the US Treasury about insuring all deposits at US banks (those over US$250,000) but this is also unlikely to actually occur as it would mean a massive fiscal hit to the government.

The outlook for equities in the near-term is constrained because there could be more strains in the banking system, global inflation has been surprising to the upside in the US and Europe which may keep central banks more hawkish than expected and the geopolitical environment remains very tense with news this week that Russia is planning to station tactical nuclear weapons in Belarus in retaliation for the UK providing Ukraine with tank shells with depleted uranium and the relationship between the US/China is deteriorating again, with further progress on the potential US TikTok ban.

Trump was indicted this week on “falsifying business records” which is related to the hush money payment to Stormy Daniels. This was not an unaccepted outcome, especially as there are three legal cases facing Trump and at least one was expected to lead to a trial. Besides the media frenzy around a potential Trump mug shot and fingerprints, the importance of this decision is around the implications for the 2024 Presidential election where Trump is planning to run. The trial for this case would not begin for over a year so it would probably start after the primary election which would give Trump a chance to run as the Republican nominee. And it may rally Trump supporters because it would embolden the view that he is being unfairly targeted. However, this indictment could be a negative for the general election if Trump wins the Republican nomination if the trial is occurring at the same time.

Back at home, the Greens party have agreed to the Federal government’s climate policy “safeguard mechanism” which aims to reduce emissions by 5% a year this decade from the top 215 emitters (of over 100,000 tonnes annually) by investing in cleaner (renewable-based) technology or purchasing carbon offsets, which will allow Australia to reach the target of a 43% reduction in emissions by 2030. Manufacturing companies are the winner from this deal while it’s a negative for the gas sector as it means some currently feasible projects won’t go ahead.

There was lots of talk this week about a potential wage breakout in Australia. The NSW Labor victory means that the 3% public service wage caps will be abolished. A lift in the cap above 4% would be problematic, especially if other state government’s followed suit but a wage cap between 3-4% would still be in line with the RBA’s 2-3% inflation target. There is also talk that the minimum wage could increase by 7% from 1 July (around the current rate of inflation). The minimum wage impacts ~200,000 workers or less than 2% of the total workforce so in itself it would not lead to a wages breakout. However, if award wages are also lifted by 7%, this would impact a much larger 20% of workers. Lifting wages by the rate of inflation will just create inflation problems down the track, lifting to more RBA interest rate hikes and higher unemployment which is bad for workers. While real wages growth in most major economies is currently negative because the headline rate of inflation is high, the good news is that inflation will slow this year and we expect headline inflation to be around 4% by the end of the year. Current wage indicators in Australia remain well anchored. Newly lodged Enterprise Bargaining Agreements (EBA’s) show that wages growth is averaging around 3.3% (see the chart below).

Source: Fair Work Commission, AMP

And newly advertised wages, according to Seek are rolling over (see the chart below).

Source: Macrobond, AMP

Economic activity trackers

Our weekly Economic Activity Trackers were roughly flat this week, as job advertisements continued to decline but hotel bookings are still holding up. The US indicator has lost some momentum since the start of the year (see the chart below) but is not negative.

Based on weekly data for eg job ads, restaurant bookings, confidence, mobility, credit & debit card transactions, retail foot traffic, hotel bookings. Source: AMP

Our inflation indicator ticked up again this week from higher commodity prices a lift in PMI price surveys however is still indicating that headline inflation should fall significantly in coming months (see the chart below).

Source: Bloomberg, AMP

Major global economic events and implications

The Fed’s preferred inflation indicator the personal consumption expenditure deflator came in below expectations for February with the headline and core index up by 0.3% over the month, with annual core inflation at 4.6% (expectations were for 4.7%), down from its peak of 5.4% in early 2022 – see the chart below. So there are further signs of inflation slowing and if you annualise the monthly change then core inflation is running at 3.7%.

Source: Macrobond, AMP

US accumulated savings fell further in February as consumers are drawing down on their savings and are now around $0.96tn, down from a peak of $2.1tn. So there are still excess savings that consumers can draw on.

Source: Macrobond, AMP

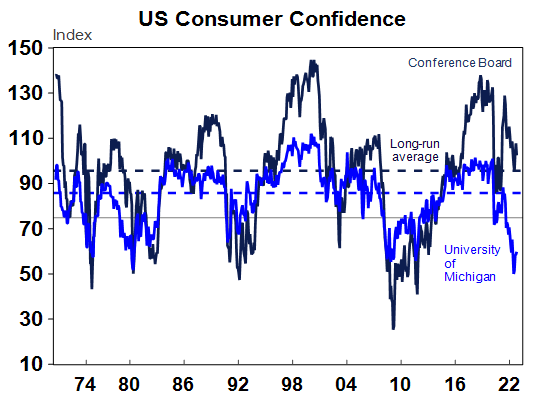

US consumer confidence, according to the Conference Board rose in March and is holding up much better than the University of Michigan consumer sentiment index (see the chart below) because the Conference Board measure is more closely aligned to labour market conditions which still remain very solid. Regional manufacturing indices were mixed (Richmond Fed manufacturing rose in March but is still negative but the Dallas Fed fell further), home prices were down by 0.4% according to CoreLogic (better than expected), pending home sales were up in February, initial jobless claims rose and so did continuing claims but they are both still at low level. Fed speakers this week indicated overall that the bias is still towards at least one more rate hike from the Fed, although a more cautious tone was evident given the issues in the banking sector.

Source: Macrobond, AMP

In Europe, the German IFO business climate survey surprised to the upside in March, rising to a 13-month high. But consumer confidence in France fell in March.

Chinese industrial profits were down by 22.9% year on year in the first two months of the year, as factories still had to recover from the Covid-lockdown slump. The official manufacturing PMI declined to 51.9 in March (from 52.6 last month) which shows that manufacturing activity is still solid and positive in China but eased up after the initial post-reopening bounce. Services activity is stronger with the services PMI up to 58.2 from 56.3 last month (see the chart below).

Source: Bloomberg, AMP

Australian economic events and implications

Australian retail sales rose by a small 0.2% in February and are down by 1.5% on a three-month average, a clear sign that consumers are pulling back on spending. The February monthly consumer price index was lower than expected, tracking at 6.8% year on year after peaking at 8.4% per annum in December and looks to be declining slightly faster than the RBA was forecasting. However, the current pace of inflation is still clearly way too high but inflation will slow further over 2023 because commodity prices have fallen, Covid-related supply chain constraints have eased and inflation is a lagging indicator of economic activity so will slow further as economic momentum has weakened and as consumers cut back spending.

Source: ABS, AMP

Australian job vacancies fell by 1.5% over the three months to February, after falling for the previous two quarters although are still 3.6% higher than a year ago and 92% higher than pre-Covid levels. There are around 0.9 open jobs for every unemployed person which is down from its highs (see the chart below) but still indicating that the labour market remains tight.

Source: ABS, AMP

Private sector credit rose by 0.3% in February and is 7.6% higher over the year with housing credit slowing, for both owner-occupiers and investors. Business credit growth also continues to turn down.

Source: RBA, AMP

What to watch over the next week?

US data next week includes construction spending (expected to be flat over February), March ISM (both manufacturing and services indices are expected to soften slightly), factory orders and payrolls (released next Friday which should show solid employment growth, but a moderation from recent months with the unemployment remaining unchanged at 3.6%). Some Fed officials speak including Kashkari, Williams, Mester and Bullard.

European data includes the February unemployment rate which is likely to remain low at around 6.6%.

In Japan the March quarter Tankan business survey should show a positive result, although a drop on last month.

In China, the Caixin manufacturing and services PMI should rise in March, given the lift in the official PMI.

In Australia, the week starts off with March CoreLogic home price data (the daily data shows that capital city home prices will increase by 0.8% over the month with Sydney up by 1.4%, Melbourne +0.6%, Brisbane +0.1%, Adelaide -0.1% and Perth +0.5%), the Melbourne Institute inflation gauge will give a guide to inflation in March, February building approvals are expected to show a rebound after a large fall in the prior month, housing finance is likely to rebound slightly and the February trade surplus is expected to be just over $10bn. The RBA’s meeting on Tuesday will be closer than markets are pricing in (there is only a 1% chance of a hike priced in) which have come down considerably since the start of the US/Europe banking crisis. Governor Lowe mentioned the key data points to watch since the last meeting including the labour force data, business and consumer surveys, retail sales and the monthly consumer price data. Overall the data shows some easing in growth momentum recently, but its coming from a high base and inflation is slowing after a peak in December 2022 at a faster pace than the RBA was expecting. Alongside the risks from the banking sector, this should be enough to get the RBA to pause. However, the Board is still likely to deliberate on raising the cash rate by another 0.25% and a tightening bias is likely to be maintained in the post-meeting statement. While we think that the RBA will keep the cash rate unchanged at its current level of 3.6% from now until the end of the year when we expect rate cuts to occur, the risk is of another hike in coming months. Governor Lowe speaks on Wednesday at the National Press Club (no topic has been listed yet). Thursday the RBA’s semi-annual Financial Stability Review is released just before the Easter public holiday break which will mention the risks to the financial system from the current banking crisis in the US and Europe and the risks to the domestic banking system along with households and businesses from higher interest rates.

The RBA review will be handed to Treasurer Jim Chalmers on Friday and it will be released in April before the Federal Budget so expect headlines around this in coming weeks.

Outlook for investment markets

The year ahead is likely to see easing inflation pressures, central banks moving to get off the brakes and economic growth weakening but stronger than feared. This along with improved valuations should make for better returns than in 2022. But as we are seeing there will be bumps on the way – particularly regarding interest rates, recession risks, geopolitical risks and raising the US debt ceiling in the September quarter.

Global shares are expected to return around 7% this year. The post mid-term election year normally results in above average gains in US shares, but US shares are likely to be a relative underperformer compared to non-US shares reflecting still higher price to earnings multiples versus non-US shares. The $US is also likely to weaken further which should benefit emerging and Asian shares.

Australian shares are likely to outperform again, helped by stronger economic growth than in other developed countries and stronger growth in China supporting commodity prices and as investors continue to like the grossed-up dividend yield of around 5.5%.

Bonds are likely to provide returns a bit above running yields, as inflation slows and central banks become less hawkish.

Unlisted commercial property and infrastructure are expected to see slower returns, reflecting the lagged impact of weaker share markets and last year’s rise in bond yields (on valuations). Commercial property returns are actually likely to be negative.

Australian home prices are likely to fall another 8% or so as rate hikes continue to impact, resulting in a top to bottom fall of 15-20%, but with prices expected to bottom around the September quarter, ahead of gains late in the year as the RBA moves toward rate cuts.

Cash and bank deposits are expected to provide returns of around 3.25%, reflecting the back up in interest rates.

A rising trend in the $A is likely over the next 12 months, reflecting a downtrend in the overvalued $US, the Fed moving to cut rates and solid commodity prices helped by stronger Chinese growth.

Diana Mousina,

Senior Economist,

AMP

31 Mar 2023

What you need to know

While every care has been taken in the preparation of this article, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent AMP. This article is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.

The information on this page was current on the date the page was published. For up-to-date information, we refer you to the relevant product disclosure statement, target market determination and product updates available at amp.com.au.